The Banque de France just dropped a number that should make anyone living in France pause: over-indebtedness dossiers jumped 9.8% in 2025. That’s nearly triple what the central bank had forecast just a year ago. For international residents already juggling currency fluctuations, visa requirements, and the infamous French bureaucracy, this trend signals something concrete, credit is getting harder to manage, and the safety nets are stretching thin.

The 10% Surge in Context

Governor François Villeroy de Galhau announced the figure during a Senate hearing, calling it a “subject of attention.” That’s French central banker speak for “we’re concerned.” The total, 134,803 dossiers filed in 2024, represents a decade-high. Yet the governor was quick to add perspective: we’re still 32% below the 2014 peak when the crise du surendettement (over-indebtedness crisis) hit its worst point.

What changed? The composition of debt, for one. Personal loans now appear in 62.2% of dossiers, while revolving credit, those open-ended lines that keep ticking, shows up in only 48.2% of cases. The shift matters: personal loans have fixed terms and clearer paths to repayment. Revolving credit, especially through services like LOA (Location avec Option d’Achat) for cars or buy-now-pay-later apps, can spiral silently.

Why Credit Is Filling the Gap

The underlying driver isn’t complicated: purchasing power isn’t keeping pace. Wages stagnate while rents, energy bills, and grocery costs climb. Many households turn to crédit à la consommation (consumer credit) not for luxury purchases, but to cover the lag between paydays and due dates. Furniture rentals, car financing, even spreading utility bills across months, what starts as convenience becomes necessity.

Discussions among financial observers point to a pattern: credit fills the gap when salaries don’t stretch. The problem isn’t just the total amount borrowed, but the multiplication of small loans. A 0% interest payment plan for a new washing machine seems harmless. Add three more “interest-free” plans, a revolving credit card for emergencies, and a LOA for the family car, and suddenly multiple lenders are deducting from the same account.

The Banque de France Response

The institution isn’t sitting idle. It has deployed additional staff to process the rising number of dossiers. More interestingly, it’s exploring “simplification and artificial intelligence” to handle the workload. For the average person, this means the process might get faster, but also that algorithms could start determining who qualifies for debt restructuring.

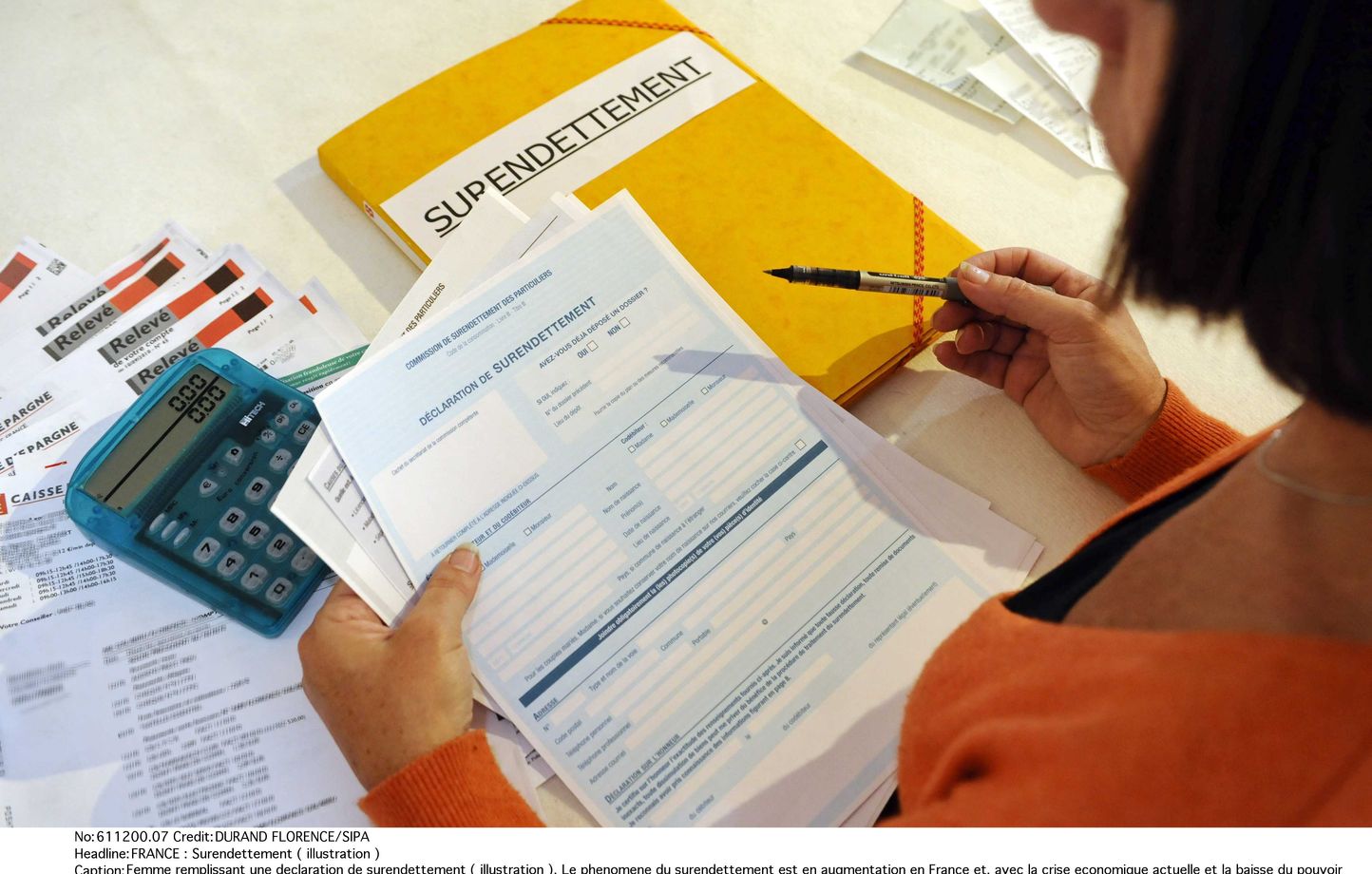

If you’re unfamiliar with the French system, here’s how it works: when you can’t meet payments, you file a dossier de surendettement with the Banque de France. The state-mandated commission then negotiates with creditors, potentially freezing interest and setting a multi-year repayment plan. It’s a powerful tool, but it also blocks access to new credit for years. The fact that more people are filing suggests either better awareness or deeper desperation, likely both.

What This Means for International Residents

Expats and international residents face unique risks. You might have income in one currency but pay bills in euros, exposing you to exchange rate swings. Your work contract might be a CDD (fixed-term contract), which lenders view as less stable. And you may not have family support to fall back on.

The 10% rise in dossiers includes people from all backgrounds. Financial advisors working with international clients report that many newcomers underestimate how quickly small French loans add up. A €3,000 furniture loan, a €5,000 car LOA, and a €2,000 credit card balance total €10,000, often at effective rates far higher than advertised.

Practical steps if you’re feeling the squeeze:

– Consolidate before filing: A single prêt personnel at 6% beats three revolving credits at 21%.

– Check your assurances: Many credit contracts include insurance that can be canceled or reduced.

– Use the simulation tools: The Banque de France offers online calculators to estimate if you qualify for a restructuring plan before you officially file.

– Talk early: Creditors prefer a call before a missed payment. Some will freeze interest for 30 days if you present a plan.

Looking Ahead: The 2026 Pressure Points

The governor’s team had expected only a 3% rise. They missed the mark because they underestimated how persistent inflation would be. For 2026, watch these triggers:

– Variable-rate mortgages resetting: Many French households took out prêts immobiliers with rates that adjust after 5-7 years. The first wave hits in 2026.

– Energy subsidies ending: Government aid for electricity and gas bills is phasing out. Real utility costs will jump.

– Transport costs: The pass Navigo (Paris region transit pass) and other public transport fees rise annually, often above inflation.

The Banque de France insists the situation remains “under control.” And statistically, they’re right, debt service ratios are still below 2008 levels. But statistics don’t pay bills. For households already using credit to bridge monthly shortfalls, a 10% rise in filings is a warning, not a comfort.

Key Takeaways for Your Financial Health in France

- Treat credit like a tax: It’s a mandatory payment that never goes away until cleared. Budget it first, not last.

- Avoid LOA for cars: The monthly payment looks low, but you own nothing and the insurance requirements are high. A used car with a standard loan often costs less long-term.

- File before the bailiff: If you miss two payments, creditors can initiate legal action. Filing a dossier de surendettement first gives you control of the timeline.

- Check your droits: As a resident, you have access to free financial counseling through associations like la finance pour tous. Use them.

The 10% surge isn’t a catastrophe, it’s a signal. French households are borrowing more to maintain standard of living. For international residents, the lesson is sharper: build a buffer in euros, not just in your home currency, and treat the French credit system with the same caution you’d treat any complex bureaucracy. It works, but it doesn’t forgive.