A 30-year-old engineer earning €45,000 per year should be able to afford a decent apartment in Marseille. Instead, he’s living with his parents in Aubagne, commuting two hours daily, and watching his savings stagnate while property prices climb 8% annually. This isn’t a rare case, it’s the new normal for France’s sacrificed generation.

The numbers are stark. According to an Odoxa survey for Nexity, 83% of young Provençaux aged 18-34 find it difficult to secure housing, placing the PACA region at the top of France’s housing crisis leaderboard. The national average sits at 61%, but in urban centers, the reality is far worse. In Île-de-France, 80% of youth struggle, while Auvergne-Rhône-Alpes follows closely at 81%. These aren’t just statistics, they’re a systemic failure reshaping life trajectories.

When "Home" Becomes a Luxury Good

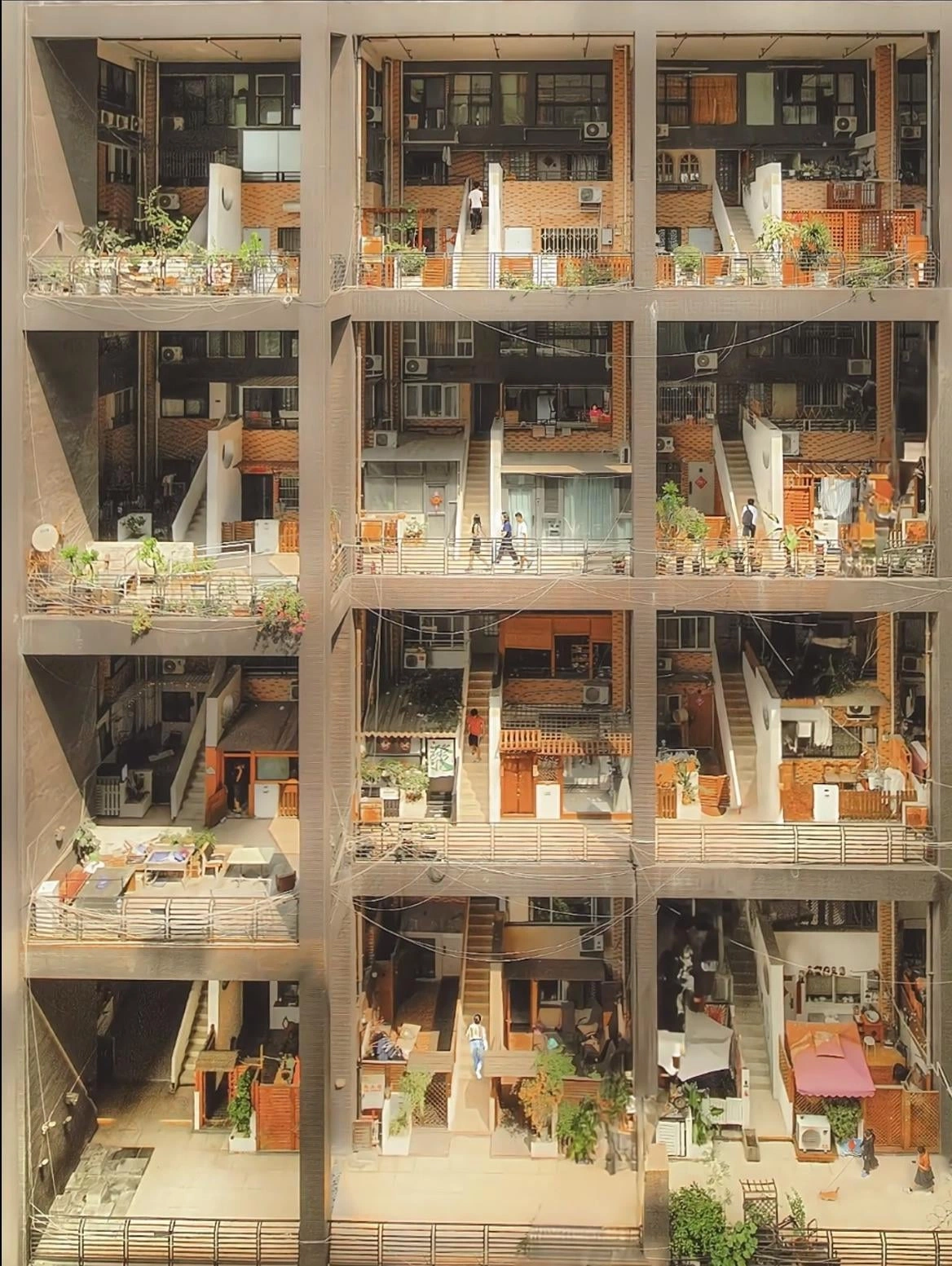

The crisis operates on two fronts: purchasing power and rental accessibility. For aspiring homeowners, the barriers are structural. 59% cite purchase prices as prohibitively high, while 41% lack sufficient down payment (apport personnel). Banks have tightened lending criteria, leaving 32% unable to meet mortgage conditions. The result? A generation of engineers, teachers, and healthcare workers permanently locked out of property ownership.

The rental market offers no refuge. 71% of young renters find rents disproportionate to their income, with 50% facing brutal competition for scarce units. In Paris, a 25m² studio in the 18th arrondissement commands €900 monthly, nearly half the net salary of a junior marketing assistant. The dépôt de garantie (security deposit) often requires parental guarantees, as the Garantie Visale program, while helpful, doesn’t cover all risk profiles.

This financial pressure creates a cascade of life-altering decisions. 36% of young Provençaux have abandoned job applications due to housing constraints, while 30% nationally have done the same. More troubling: 21% have given up on having children, and 20% have postponed relationships. Housing has shifted from a foundation for life to a barrier against it.

The "Renoncement" Effect: From Emancipation to Abdication

Véronique Bédague, CEO of developer Nexity, captured the generational mood: "Housing was a factor of emancipation. It has become a factor of renoncement (renunciation)." The word choice is deliberate, this isn’t mere delay, but active surrender of life plans.

Young couples now occupy apartments averaging 18m², making the addition of a child physically impossible. The parliamentary mission on birth rates, launched in June 2025, identified housing as the third-largest obstacle to family formation after financial concerns (39%) and job insecurity (21%). When your kitchen doubles as a home office and dining room, planning for a nursery becomes fantasy.

The psychological toll is measurable. 86% of young people report mental health impacts from housing stress, while 72% see it eroding social cohesion. Many describe a persistent sense of precarity, even with stable employment. As one young professional noted, the uncertainty of geopolitical tensions and AI-driven job disruption makes a 25-year mortgage feel like signing a contract with quicksand.

The Boomer Millstone and Generational Wealth Chasms

Intergenerational tension simmers beneath the surface. Many older French, beneficiaries of post-war housing policies and price appreciation, view the crisis through a distorted lens. Some suggest that young people living with parents are "building wealth" through forced savings, a perspective that ignores the opportunity costs of delayed independence.

The reality is harsher. 28% of a median salary already funds pensions through social contributions, leaving little room for saving. Meanwhile, boomers cling to properties, expecting "la pierre" (real estate) to deliver windfall profits. This creates a market where supply is artificially constrained, as empty-nesters occupy 3-bedroom apartments while young families cram into studios.

The viager (life estate) system, where buyers pay a lump sum and monthly payments to elderly sellers who remain in the property, exemplifies the generational transfer problem. While innovative, it concentrates wealth further and does little to address the core supply shortage.

Policy Theater: Why Government Solutions Miss the Mark

The French government hasn’t been idle, but interventions often feel like applying bandages to a hemorrhage. The Prêt à Taux Zéro (PTZ) (zero-interest loan) helps some primo-accédants (first-time buyers), but its complex eligibility criteria exclude many middle-income youth who earn too much for aid yet too little for market rates.

Proposals to revive APL accession (homeowner housing assistance) show promise, covering up to 25% of mortgage payments for modest households. Yet this represents just 6% of total housing aid, a fraction of what’s needed. Economists like Pierre Madec of OFCE argue for broader solvency support, noting that rent control in tense zones prevents aid from inflating rents.

The 1 Jeune 1 Solution platform centralizes resources, and Garantie Visale covers deposits, but these are navigation tools, not supply solutions. The core issue remains: France builds 300,000-400,000 units annually while needing 500,000+. Construction costs rose 15% in 2025, and restrictive zoning laws prevent dense urban development.

The Debt Spiral and Financial Contagion

Housing costs are pushing young households into precarious financial positions. The Banque de France reported that over-indebtedness filings jumped 9.8% in 2025, nearly triple forecasts. This aligns with findings that 54% of young Provençaux cut food budgets to afford rent, while some forego medical care.

This isn’t just a youth problem, it threatens systemic stability. When your highest-earning young workers can’t afford to live near jobs, talent migration accelerates. Some engineers are retraining as teachers for €2,000 net monthly, accepting permanent tenancy as their ceiling. Others join the FIRE movement (Financial Independence, Retire Early), but not by choice, it’s a survival strategy when traditional paths collapse.

For international residents, the calculus is even more brutal. Without parental guarantees or French salary history, securing a bail (lease) is nearly impossible. Many resort to short-term furnished rentals at 40% premiums, further eroding savings potential.

What Actually Works: Strategies for the Sacrificed Generation

Despite the bleak landscape, some navigate successfully. The key is abandoning conventional wisdom:

1. Geographic Arbitrage

Stop chasing Paris or Lyon. Cities like Nantes, Lille, and Montpellier offer 30-40% lower prices with strong job markets. Remote work enables this shift, if your employer permits it. The Mobilité programs through Crous and Fac-Habitat provide transitional housing for those relocating.

2. Collective Buying

Young professionals are forming SCI (Société Civile Immobilière) partnerships to purchase multi-unit buildings collectively. This shares costs and risks, though it requires watertaught legal agreements. The Fac-Habitat model, with 12,000 student housing units across 65 cities, demonstrates how collective structures can bypass market failures.

3. Leverage Every Aid Mechanism

- APL: Up to €250/month for eligible renters

- RSA jeunes actifs: For those under 25 with limited income

- Complementaire Santé Solidaire (CSS): Reduces health costs, freeing housing budget

- Crous emergency aid: One-time grants for students in crisis

4. Negotiate Total Compensation

When salaries can’t rise, negotiate aide au logement (housing assistance) from employers. Some tech companies now offer €300-500 monthly housing supplements, recognizing that talent retention requires addressing this crisis.

5. Consider the "Access" Model

Cogedim’s Access program in Villeneuve-la-Garenne shows innovation: €500 down payments, delayed repayment until move-in, and compact units at €6,000/m² (vs €10,000+ in central Paris). While small (40m² T2 apartments), they enable ownership at monthly costs equivalent to rent.

The Hard Truth: This Won’t Fix Itself

The housing crisis isn’t a temporary market correction, it’s a structural rupture. Véronique Bédague warns the worst is ahead: "La crise est devant nous" (The crisis is before us). With construction permits down 12% in 2025 and interest rates stabilizing above 3%, relief isn’t imminent.

For young French and international residents alike, this means hard choices. Either accept a lower quality of life in peripheral cities, leverage every available aid program, or consider leaving France entirely, a choice more are making as housing costs exceed quality-of-life benefits.

The generation entering adulthood today faces a France where housing is no longer a right or even a commodity, but a luxury good. Until policymakers treat this as the emergency it is, streamlining construction laws, taxing vacant properties aggressively, and massively increasing social housing, the sacrificed generation will continue to pay the price through deferred dreams and diminished lives.

Internal Links for SEO:

– Learn how rising interest rates silently reduce buying power without salary changes

– Understand why cultural pressure to buy property clashes with today’s unaffordable market

– See how rising household debt levels signal worsening financial strain on young adults

– Explore why young workers are losing faith in traditional systems and seeking financial independence early

– Discover the growing financial despair pushing young French toward extreme frugality and early retirement movements