Every March, thousands of international residents in the Netherlands stare at their Belastingdienst (Tax Authority) screens with the same expression: pure confusion. They’ve been diligently stashing money in their DeGiro pension investment accounts, expecting that sweet tax deduction. Yet when the annual tax return rolls around, the numbers don’t add up, the terminology looks like alphabet soup, and that promised belastingvoordeel (tax advantage) seems to evaporate.

The problem isn’t DeGiro. It isn’t even the Belastingdienst, really. The issue is that Dutch pension tax law operates like a three-dimensional chess game where the pieces are labeled in bureaucratic Dutch. Most expats and international workers are playing checkers.

Why Factor A Is the Red Herring Ruining Your Deduction

Here’s where nearly everyone trips: that “Factor A” field staring at you from the pension section of your tax return. Your gut says “this is where my pension contributions go.” Your gut is wrong, and this mistake costs people hundreds, sometimes thousands, in missed deductions.

Factor A represents your werkgeverspensioen (employer pension) growth from the second pillar (tweede pijler). The money you shovel into DeGiro’s pension account? That’s lijfrente (annuity), falling under the third pillar (derde pijler). The Belastingdienst treats these as entirely different animals, and conflating them is like trying to claim cat food expenses on your dog’s veterinary insurance.

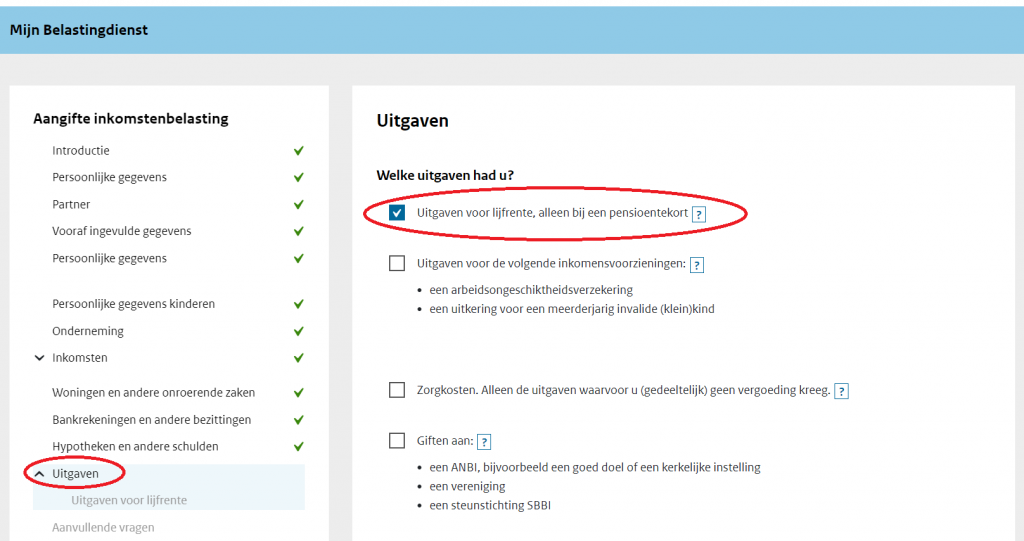

As BrightPensioen explains in their tax guide, when you see “pensioen”, “Factor A”, or “pensioenaangroei” on your return, you must mentally tag it as “not my DeGiro money.” The actual lijfrente deduction hides elsewhere, buried under “Uitgaven” (Expenses) in a section so specific it sounds like a legal disclaimer: “Uitgaven voor lijfrente, alleen bij een pensioentekort” (Expenses for annuity, only with a pension shortfall).

The Pre-Filled Data Problem That DeGiro Users Keep Discovering

Many DeGiro users report their contributions appearing pre-filled in the tax return. Others find nothing. Both groups make expensive mistakes.

If your data is pre-filled, you must verify it against your DeGiro jaaroverzicht (annual statement) down to the cent. The Belastingdienst receives information from financial institutions, but glitches happen. Some users have reported seeing duplicate entries, both their pension and regular investment accounts listed separately, requiring manual correction.

If your data isn’t pre-filled, you must manually enter your pension account number and the exact amount contributed in the tax year. This is where people give up, assuming they’ve misunderstood the system. They haven’t. The system just demands precision that feels punitive.

The confusion intensifies because DeGiro’s pension account statements don’t scream “this is your lijfrente!” in plain English. You need to locate the specific contribution amount for the tax year, not the current value, not the gains, just what you actually deposited.

Jaarruimte and Reserveringsruimte: The Time-Traveling Deduction

Now we enter the real wormhole: jaarruimte (annual allowance) and reserveringsruimte (carry-forward allowance). These concepts determine how much you can deduct, and they’re calculated using income and pension data from two years ago.

For your 2025 tax return (filed in 2026), you need:

– Your 2025 contributions (what you actually put in)

– Your 2024 UPO (Uniform Pensioenoverzicht – Uniform Pension Overview) from your employer pension

– Your 2024 income

The jaarruimte is what you could have contributed in 2025 with tax benefit. The reserveringsruimte is unused jaarruimte from the past 10 years that you can still use. Since 2023, you can tap into a full decade of unused allowance, a potentially massive deduction that most people miss entirely.

Many expats express frustration at needing historical documents. If you’ve lost your UPO from years past, log into your pension provider’s portal. Most maintain a table of Factor A values for the previous 10 years, saving you from archaeological digs through old paperwork.

The Hidden Box 3 Trap Waiting for Pension Investors

Here’s the kicker that transforms confusion into financial pain: your DeGiro beleggingsrekening (investment account) and your DeGiro pensioenrekening (pension account) get taxed completely differently. Mix them up and you’ll either overpay Box 3 vermogensbelasting (wealth tax) or underclaim your lijfrente deduction.

Your pension account grows tax-free until retirement. Your regular investment account gets hit with Box 3 taxes on the value above the heffingsvrij vermogen (tax-free allowance), currently €57,684 for individuals, €115,368 for fiscal partners.

The 2025 tax return introduces another twist: you can now report your werkelijke rendement (actual return) instead of the fictional percentage. If your DeGiro portfolio tanked last year, this can significantly reduce your Box 3 bill. But this option only appears if you navigate the initial lijfrente section correctly.

For those exploring investment tax optimization strategies, understanding this distinction between pension and investment accounts becomes critical. The wealth tax impact on retirement planning is substantial enough that misclassification could derail your entire financial timeline.

Step-by-Step: Where to Actually Click on belastingdienst.nl

Let’s cut through the noise with the exact navigation path:

- Log into your aangifte (tax return) at belastingdienst.nl

- Navigate to “Uitgaven” (Expenses)

- Select “Uitgaven voor lijfrente, alleen bij een pensioentekort”

- If pre-filled: verify the account number and amount against your DeGiro jaaroverzicht

- If empty: manually enter your pension account number and 2025 contribution total

When the system asks: “Hebt u in 2025 pensioen opgebouwd?” and “Hebt u in 2025 premies betaald voor een nettopensioen?”, answer “nee” unless you have an actual employer pension. These questions refer to tweede pijler, not your lijfrente.

For reserveringsruimte, when asked “Wilt u niet-gebruikte jaarruimte benutten?” select ‘ja’ and choose the specific years. Use BrightPensioen’s or other calculators to determine your exact unused allowance per year.

The DeGiro-Specific Quirks No One Mentions

DeGiro users face unique challenges. The platform’s pension account is relatively new, and its integration with Dutch tax systems isn’t seamless. Some users report contributions appearing automatically, others wait weeks for statements. The key is downloading your official jaaroverzicht from DeGiro’s document center, not relying on the app summary.

If you contributed in early 2026 for the 2025 tax year (allowed until July 1), those contributions belong on your 2026 return, not 2025. Many miss this timing rule and claim the wrong year’s contributions.

Also, DeGiro’s valutakosten (currency exchange costs) of 0.25% directly impact your Box 3 returns if you’re reporting actual performance. For frequent traders in foreign assets, this can create a noticeable drag that should be factored into your werkelijk rendement calculation.

What If You Already Filed Wrongly?

Discovering this after submitting your return isn’t catastrophic. You can file a suppletie (supplementary return) within three years. The Belastingdienst will recalculate, and you’ll receive the missed refund. Interest on late refunds is minimal, better to fix it than leave it.

For those just starting, this complexity underscores why selecting investment platforms requires looking beyond fees. Tax integration and customer support for Dutch residents matter enormously.

Final Checklist: Don’t Leave Money on the Table

- Separate your accounts: Pension (tax-deferred) vs investments (Box 3)

- Locate the right section: Uitgaven → lijfrente, not the Factor A fields

- Verify pre-filled data: Match exactly to your DeGiro jaaroverzicht

- Calculate reserveringsruimte: Check the past 10 years, this is where the big deductions hide

- Time your contributions: 2025 money goes on 2025 return, even if deposited in early 2026

- Consider Box 3 optimization: Report actual returns if they beat the fictional rates

The Dutch pension tax system doesn’t care about your confusion. It cares about precise classification. Get it right once, and you’ll maximize deductions while building retirement wealth. Get it wrong, and you’re funding the treasury with money that should be funding your future.

The recent Box 3 tax reform implications only make this more urgent. As the system shifts toward taxing actual returns, properly classifying your pension versus investment accounts becomes the difference between financial optimization and accidental self-sabotage.