Most wealth building guides for young Dutch professionals follow the same predictable formula: build an emergency fund, pay off debt, stuff money into your pensioen (pension), buy a house, then maybe invest what’s left. It sounds responsible. It looks neat on a flowchart. And it’s about as effective as using a bicycle to cross the Noordzee (North Sea), technically possible, but you’re ignoring better options.

The reality of vermogensopbouw (wealth building) in the Netherlands is messier, more strategic, and heavily dependent on how you navigate specific Dutch financial structures that most advice glosses over. Let’s tear apart the conventional wisdom and rebuild something that actually works for young professionals facing a housing crisis, rising Box 3 taxes, and an AOW (state pension) age that keeps creeping upward.

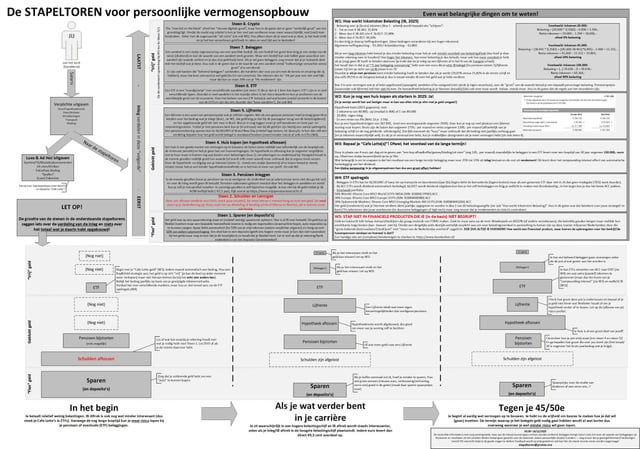

The Traditional Model: Safe, But Incomplete

The standard Dutch approach treats wealth building like a linear assembly line: salaris (salary) → sparen (saving) → pensioen (pension) → huis (house) → beleggen (investing). This model works fine if your goal is financial mediocrity and you never question the system. It fails spectacularly if you want actual financial independence before you’re 70.

Many young professionals follow this path because it’s what their parents did. The problem? Their parents bought houses when Amsterdam apartments cost less than a Tesla, and pension funds actually delivered predictable returns. Today’s reality involves bidding wars, negative real interest rates on savings, and a Box 3 tax system that punishes cash hoarding.

The model also assumes you’re a traditional employee with a stable baan (job) and a generous werkgeverspensioen (employer pension). For the growing number of freelancers, contractors, and entrepreneurs, this framework is about as useful as a chocolate teapot.

Pension First or ETFs First? The Tax Math That Divides Dutch Investors

Here’s where Dutch financial advice gets spicy. Conventional wisdom says max out your pensioen (pension) contributions before touching ETFs. The math seems compelling: you get immediate aftrek (deduction) against your box 1 income tax, often at 40% or higher, plus decades of tax-free growth. A €1 netto (net) contribution can become €1.67 bruto (gross) working for you immediately.

But this ignores a critical factor: liquidity. Once money enters most Dutch pension vehicles, it’s locked until your official pension date (currently 67, rising to 67+ months after 2028). If you lose your job at 45, want to start a business, or need cash for a medical emergency, that pension money might as well be on Mars.

Many financially savvy young professionals argue for flipping the script: build a substantial ETF portfolio first, then add pension contributions later when your income stabilizes. The reasoning? ETFs in a regular brokerage account remain accessible. You can sell them during a crisis, use them as collateral, or tap them for opportunities. Yes, you’ll pay Box 3 vermogensrendementsheffing (wealth tax) annually, but you maintain control.

The counterargument points to behavioral risk. Having easily sellable ETFs means you might panic-sell during the next crisis, locking in losses. Pension money, being locked away, forces discipline. Both sides have merit, but the “pension first” crowd often underestimates how much flexibility matters when you’re building a career in a volatile economy.

The Mortgage Payoff Trap: Why Dutch Banks Love Your Extra Payments

Dutch banks actively encourage extra hypotheek (mortgage) payments, framing it as “financial security.” What they don’t emphasize is the math behind the hypotheekrenteaftrek (mortgage interest deduction). With HRA, a 4% mortgage actually costs you around 2% net if you’re in a high tax bracket.

Paying off that mortgage early means you’re getting a guaranteed 2% return while potentially missing out on 7-10% average stock market returns. The bank benefits because you’ve reduced their risk while they could have lent that money to someone else at higher rates.

The argument for accelerated payoff relies heavily on psychological comfort. Owning your home free-and-clear feels safe. But financially, it’s often suboptimal, especially with the current low interest environment. The only scenarios where aggressive payoff makes sense: your mortgage rate exceeds 5%, you’re underwater on the property and want to reduce risk, or you’re close to retirement and prioritizing cash flow over growth.

For young professionals, that extra money typically belongs in ETFs, not in reducing a cheap loan that the government subsidizes through tax policy.

The Entrepreneur’s Perspective: Why Cash Flow Beats Savings

One of the most insightful critiques of traditional Dutch wealth building comes from entrepreneurs who point out a fundamental flaw: the model focuses on saving from salary rather than building assets that generate cash flow.

The traditional approach: work for 40 years, save 10-15% of your income, retire at 67+ with a modest pension and paid-off house. The entrepreneur’s approach: build a business, acquire rental property, create intellectual property, or develop skills that command premium rates. These assets generate cash flow that grows independently of your labor.

A freelance developer who builds a SaaS product on the side isn’t just saving €500 monthly, they’re creating an asset that could generate €5,000 monthly while they sleep. A young professional who buys a duplex, lives in one unit and rents the other, has tenants paying their hypotheek (mortgage) while the property appreciates.

The Dutch tax system actually favors this approach through various ondernemersaftrekken (entrepreneurial deductions) and the ability to build wealth inside a holding structure. Yet most standard advice ignores these pathways entirely because they’re designed for employees, not wealth builders.

Box 3: The Silent Wealth Killer You Need to Plan Around

Box 3 is where many young Dutch investors get blindsided. You pay vermogensrendementsheffing (wealth tax) on your assumed returns, not your actual returns. For 2025, the tax-free allowance is €57,000 per person (€114,000 for fiscal partners), but anything above that gets taxed on a fictional 6.04% return.

This means if your ETFs return 3% in a bad year, you still pay tax as if you earned 6.04%. Conversely, in a great year where you earn 15%, you only pay tax on the assumed 6.04%. The system is designed to be simple for the Belastingdienst (Tax Authority) but creates perverse incentives.

Smart wealth builders structure around Box 3. They max out their box 1 pension space first (because it’s Box 3-exempt), consider box 2 structures for business investments, and strategically use their hypotheek (mortgage) to reduce taxable wealth. Some even relocate assets to a holding company, though this comes with its own complexity.

The key insight: don’t just focus on returns. Focus on after-tax, after-inflation returns. A 7% ETF return becomes ~5.5% after Box 3 tax, which barely beats inflation. This makes pension contributions and other tax-advantaged structures far more attractive than they first appear.

AOW Age Increase: The Timeline Shift Nobody’s Talking About

The AOW age rising to 67 years and 3 months after 2028 might seem minor, but it fundamentally changes calculations for anyone under 40. Those extra three months require roughly €9,000-15,000 in additional savings to cover expenses, assuming €3,000 monthly spending.

More importantly, it signals that future increases are likely. If you’re 25 now, betting on retiring at 67 is naive. Planning for 70 or even 72 is more realistic. This extends your investment horizon by years, allowing more aggressive allocation to aandelen (stocks) and less to bonds.

The extended timeline also means you need more liquid assets. If you want to retire at 60, you must fund a decade of living expenses before AOW kicks in. That’s not happening with locked pension money alone. You need substantial ETF holdings or cash-flowing assets to bridge the gap.

This reality check pushes young professionals toward the ETF-first strategy. Pension contributions remain valuable, but they can’t be your only tool if you want financial independence before the government says you’re allowed to have it.

Building Your Actual Strategy: A Tiered Approach

Forget linear models. Effective vermogensopbouw (wealth building) for young Dutch professionals requires parallel tracks:

Tier 1: The Security Layer (Months 1-12)

- Build a €5,000-10,000 noodpot (emergency fund) in a regular savings account

- Pay off high-interest debt (credit cards, personal loans)

- Get adequate insurance (aansprakelijkheidsverzekering, disability)

Tier 2: The Flexibility Layer (Years 1-5)

- Max out any employer pension matching (free money)

- Then prioritize ETFs in a regular brokerage account

- Target 70-80% aandelen (stocks), 20-30% bonds, diversified globally

- Build to €50,000-100,000 for maximum flexibility

Tier 3: The Tax Optimization Layer (Years 5-15)

- Once you have solid ETF foundation, max out jaarruimte (annual pension allowance)

- Consider lijfrente (annuity) products for additional box 1 space

- Evaluate real estate if market conditions and personal situation allow

Tier 4: The Acceleration Layer (Years 10+)

- Explore onderneming (business) structures

- Consider vastgoed (real estate) for cash flow

- Optimize for Box 2 or holding structures

- Fine-tune based on actual results and changing tax laws

This approach gives you immediate security, medium-term flexibility, and long-term tax efficiency. It acknowledges that your 25-year-old self needs different tools than your 40-year-old self.

The Crypto Question: Speculation vs Strategy

The original strategy diagram controversially included crypto as a final wealth building step. The community response was immediate and harsh: crypto belongs in the “speculation” bucket, not legitimate wealth building.

They’re right. Crypto isn’t an asset that generates cash flow or has intrinsic value. It’s a speculative instrument where your returns depend entirely on someone else paying more later. That doesn’t mean you should avoid it entirely, but limit exposure to 1-5% of your portfolio at most.

Treat crypto like going to the casino: only spend what you can afford to lose completely. Your core vermogensopbouw (wealth building) should happen in regulated, taxed, transparent instruments like ETFs, pension funds, and real estate.

What the Experts Won’t Tell You: The Housing Market Reality

Many wealth building frameworks assume you’ll buy a house. In 2025 Netherlands, that’s a dangerous assumption. With average Amsterdam prices over €7,000 per square meter and strict hypotheek (mortgage) requirements, many young professionals are priced out.

The uncomfortable truth: renting and investing the difference often beats forced homeownership in overpriced markets. The math is complex and depends on rent vs buy ratios, but don’t assume buying is always the right move. Sometimes, building a massive ETF portfolio while renting a cheap apartment is the faster path to financial independence.

This challenges deeply held Dutch cultural beliefs about eigenwoningbezit (homeownership), but financial independence requires following math, not tradition.

Final Word: Your Strategy Should Evolve With You

The most important takeaway: there’s no universal blueprint. A 23-year-old software engineer in Amsterdam needs a different strategy than a 28-year-old freelancer in Groningen or a 25-year-old corporate lawyer in Rotterdam.

Start with flexibility. Build liquid ETF investments while keeping costs low. As your income grows and life becomes more stable, shift toward tax optimization through pension contributions. Consider real estate only when the numbers make sense for your specific situation, not because “everyone should own a house.”

And critically, understand that potentiële valkuilen met Box 3 en pensioenplanning can trap you in a system designed for industrial-era employment when you’re trying to build 21st-century wealth. The Dutch system rewards those who understand its quirks and punish those who follow generic advice.

The best strategy? Build enough liquid wealth to have options, then optimize for taxes. Everything else is just details.

Actionable Steps This Week:

- Calculate your actual net worth and Box 3 exposure

- Check your pension jaarruimte (annual allowance) at mijnpensioenoverzicht.nl

- Open a low-cost brokerage account if you don’t have one

- Run the numbers on your mortgage: would extra payments beat investing after HRA?

- Join a community like r/geldzaken to see real experiences, not just theory

The Dutch wealth building game isn’t about following a pretty diagram. It’s about understanding the rules well enough to know when to break them.