You’re locked into a CHF 7,258 annual payment for the next two decades. Your money grows at a snail’s pace, swallowed by fees. And the kicker? You can’t move it without blowing up your mortgage. Welcome to the dark side of Switzerland’s beloved indirekte Amortisation (indirect amortization) system.

A recent case making waves in Swiss financial circles tells a familiar story: a homeowner discovered their insurance-based Säule 3a (Pillar 3a) product, pledged against their Hypothek (mortgage) with AXA, couldn’t be replaced with a more attractive bank solution from VIAC. The mortgage wasn’t due for renewal for years. The result? A financial straitjacket disguised as prudent planning.

The Swiss Mortgage-3a Nexus: How We Got Here

Indirect amortization through Pillar 3a is Switzerland’s tax-optimized answer to mortgage repayment. Instead of paying down your mortgage directly, you contribute to your Pillar 3a account and use the accumulated capital to reduce the mortgage debt later. This approach keeps your mortgage interest high, maximizing your tax deductions, while building retirement savings.

The math is seductive. In 2026, you can contribute up to CHF 7,258 annually (with a pension fund) or 20% of net income (max CHF 36,288) without one. Every franc reduces your taxable income, potentially saving hundreds or thousands in taxes each year. For homeowners in high-tax cantons like Zurich, Geneva, or Basel, this is serious money.

But here’s where the Swiss system reveals its split personality. Pillar 3a comes in two flavors: bank accounts with investment flexibility, and insurance policies that bundle retirement savings with risk coverage. Once you pledge that insurance product to your mortgage lender, you’ve entered a world of restrictions that most financial advisors gloss over during the initial consultation.

The Insurance Trap: When “Security” Becomes a Ball and Chain

Insurance companies market their 3a products as the responsible choice. You get death and disability coverage alongside retirement savings. If tragedy strikes, the insurance pays off your mortgage, protecting your family. It’s a compelling pitch, especially for young families stretching their budgets to afford Swiss real estate.

The reality? You’re signing a long-term contract with exit penalties that make mobile phone providers look generous. These products typically offer lower returns than bank alternatives, with high administrative fees and surrender charges that can eat up years of contributions.

More critically, major lenders like AXA refuse to accept bank-based 3a solutions as collateral for indirect amortization. They want the risk coverage that insurance products provide. This creates a vendor lock-in: once you’ve pledged an insurance 3a to your mortgage, switching to a more profitable bank solution becomes nearly impossible until your mortgage renewal date.

And those renewal dates? In Switzerland, they come every five, ten, or fifteen years depending on your fixed-rate term. Miss your window, and you’re trapped for another half-decade or more.

The Bank Alternative: What You’re Missing

While your money languishes in an insurance product, bank-based 3a solutions, especially the popular VIAC, Finpension, or Frankly offerings, let you invest in global equity funds with fees as low as 0.0% to 0.5%. Historical returns on these platforms have averaged 6-8% annually over the past decade, compared to the 1-2% typical of insurance products after fees.

The difference is stark. Over 20 years, a CHF 7,258 annual contribution growing at 7% becomes roughly CHF 316,000. At 1.5%, it becomes CHF 168,000. That’s a CHF 148,000 opportunity cost, enough to fund several years of retirement or pay for your children’s university education.

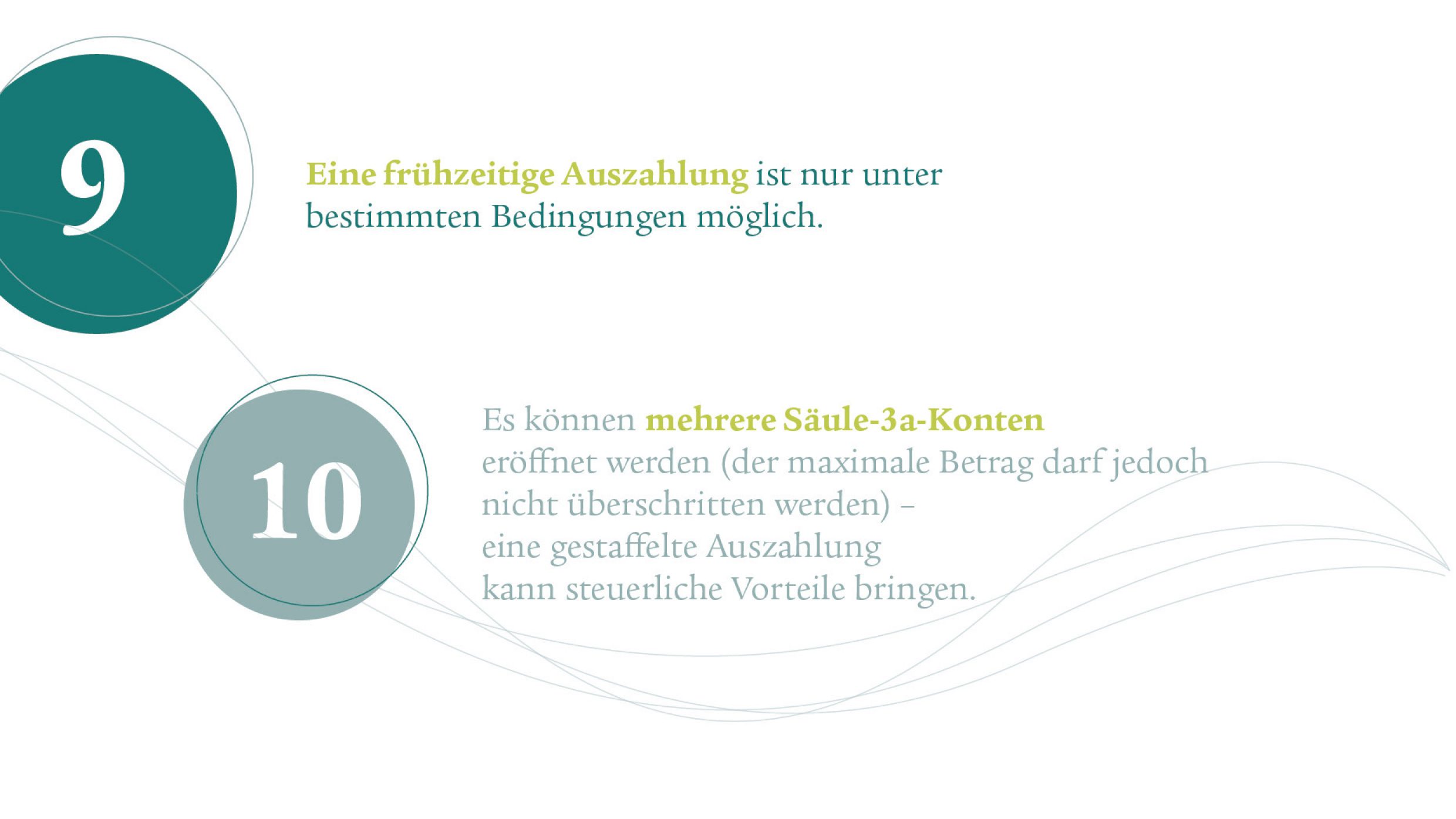

Bank solutions also offer flexibility. You can adjust contributions annually, pause them during financial hardship, or withdraw early for specific purposes like buying property or leaving Switzerland. Insurance products? They demand rigid annual payments, and early withdrawal triggers penalties that can wipe out your gains.

The Risk Coverage Question: Do You Actually Need It?

Insurance companies argue their risk coverage justifies lower returns. But let’s examine what you’re really buying.

For a 35-year-old with a CHF 800,000 mortgage, disability coverage through a standard insurance policy might cost CHF 1,500-2,000 annually. Death coverage is often cheaper. Meanwhile, the return difference between insurance and bank 3a products can cost you CHF 3,000-4,000 annually in lost investment growth.

You could purchase standalone risk coverage separately and still come out ahead financially. Many financial advisors, especially those not earning commissions from insurance sales, recommend this approach. You maintain investment flexibility while securing necessary protection at lower cost.

The catch? Once your mortgage is pledged to an insurance 3a, your lender has no incentive to let you switch. They’ve assessed your risk profile based on that coverage. Removing it triggers a new risk assessment, which could affect your interest rate or even your mortgage eligibility.

The Renewal Gamble: Timing Your Escape

Swiss mortgage terms create natural exit points. According to NZZ analysis, you should start planning 12-18 months before your mortgage expires. This gives you time to shop around, negotiate with multiple lenders, and secure favorable terms.

If you’re currently locked into an insurance 3a, mark your calendar for two years before your mortgage renewal. That’s when you need to start:

1. Building cash reserves outside your 3a to demonstrate financial stability

2. Researching alternative risk coverage options

3. Negotiating with potential new lenders who might accept bank 3a solutions

4. Calculating whether breaking the insurance contract early (and paying penalties) could still be profitable long-term

Some lenders, particularly smaller regional banks and insurance-linked mortgage providers, are more flexible than giants like AXA. During the 2024-2025 period, several Swiss mortgage brokers reported success in negotiating transitions for clients with strong financial profiles.

Breaking Free: Strategies for the Trapped

Strategy 1: The Parallel Account

Open a separate bank-based 3a account for new contributions while keeping the insurance product pledged. You won’t get the tax advantage on the full CHF 7,258, but you can still invest additional retirement funds optimally. This hybrid approach is gaining popularity among financially savvy homeowners.

Strategy 2: The Early Renewal

Some lenders allow early renewal for a fee, typically 0.5-1% of the mortgage value. On a CHF 800,000 mortgage, that’s CHF 4,000-8,000. If you can save more than that in improved investment returns over the remaining term, it makes mathematical sense.

Strategy 3: The Risk Replacement

Purchase standalone disability and life insurance policies, then negotiate with your lender to release the insurance 3a pledge. This requires a strong financial position and cooperative lender, but it’s increasingly feasible as competition heats up in the Swiss mortgage market.

Strategy 4: The Waiting Game

If your mortgage renewal is within 3-5 years, do the math. Calculate your opportunity cost of staying versus the friction of switching. Sometimes, biting the bullet and waiting for the natural renewal window is the least-bad option.

The New Rules: A Glimmer of Hope

Starting in 2026, Switzerland introduces retroactive Pillar 3a contributions. You can fill gaps in your 3a history for up to ten years, paying missed contributions in addition to your current annual maximum. For homeowners who’ve been under-contributing due to insurance product dissatisfaction, this offers a chance to supercharge a new bank-based 3a once they escape the mortgage pledge.

The rule change also pressures insurance companies to improve their offerings. When customers can catch up on contributions later, the “use it or lose it” urgency that drives insurance sales diminishes.

The Bottom Line: A Question of Control

The mortgage-linked Pillar 3a controversy boils down to one issue: control. Insurance products transfer control to the provider. You sacrifice returns and flexibility for perceived security. Bank products keep you in the driver’s seat but require discipline and separate risk management.

For most Swiss homeowners under 50, the math favors bank solutions with separate risk coverage. The compounding advantage is simply too large to ignore. But the system’s design, where lenders dictate collateral requirements, creates a coordination problem that individual borrowers struggle to solve.

Your move? If you’re house-hunting or refinancing, insist on mortgage terms that accept bank-based 3a pledges. Shop lenders aggressively. And if you’re already trapped, start planning your exit strategy today. That renewal date isn’t as far away as it seems.

The Swiss financial system works brilliantly, until it doesn’t. The mortgage-linked Pillar 3a trap is one of its most profitable blind spots for insurers and most expensive mistakes for homeowners. Don’t let the promise of “security” cost you your financial freedom.