Refinancing Fever in France: Are You About to Make a €10,000 Mistake?

Your neighbor just shaved €200 off his monthly mortgage payment. Your colleague bragged about locking in a "historically low" rate. The pressure is building, and your bank advisor keeps leaving voicemails about "optimizing your financial situation." Welcome to France’s refinancing wave of 2026, where homeowners who borrowed at 2023’s peak rates are now scrambling to capitalize on a modest but meaningful rate retreat.

But here’s what the headlines don’t tell you: the difference between a smart refinancing move and an expensive miscalculation often comes down to three French banking quirks that most international residents never learn until it’s too late.

The Math That Matters: When 1.16% Is Worth €10,000

Let’s cut through the noise with real numbers. In early 2025, many French borrowers signed mortgages at 4.36% over 25 years. Today, February 2026, rates for solid profiles hover around 3.2%, a 1.16% spread that sounds substantial. On a €200,000 loan, that difference translates to roughly €135 less per month, or €40,500 over the full term.

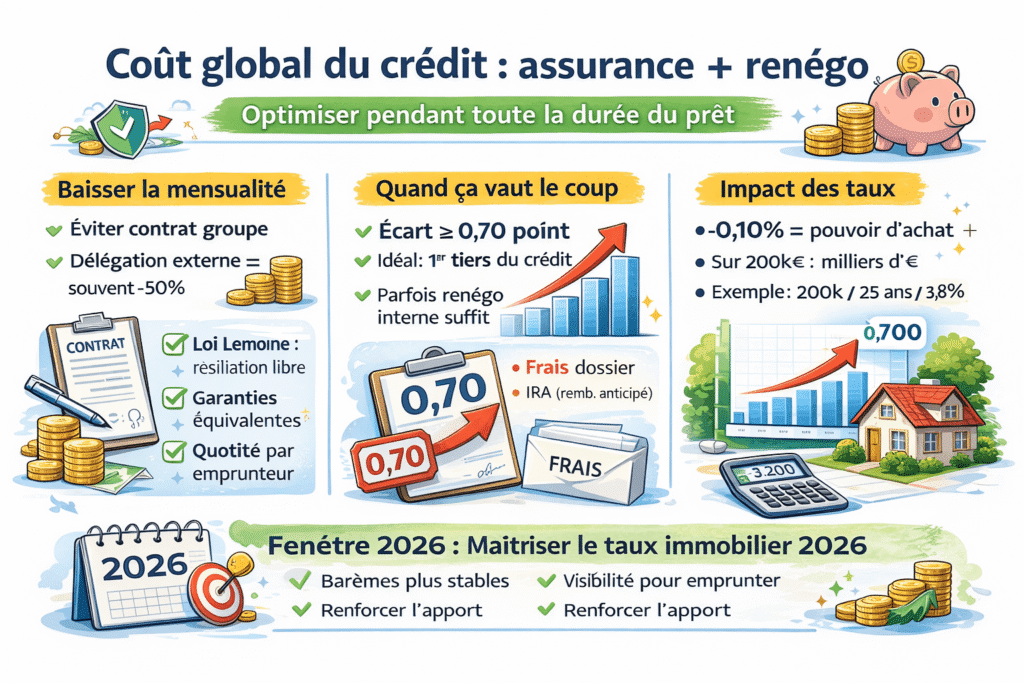

However, the refinancing threshold that French banks actually respect is much narrower than you might think. According to recent market analysis, the operation only becomes profitable with a minimum rate differential of 0.70%, and that’s before factoring in the hidden costs that can turn your supposed savings into a financial mirage.

The real kicker? Your loan’s remaining duration determines everything. If you’re beyond the first third of your repayment schedule, the mathematics of refinancing start working against you. You’ve already paid the bulk of interest charges upfront through France’s amortization structure, meaning each year that passes reduces your potential gain.

Why Your Bank Is Suddenly So Accommodating

French banks aren’t lowering rates out of generosity. The European Central Bank’s (BCE) monetary policy has created a complex dynamic where lending institutions are caught between competing pressures. On one side, the BCE’s rate decisions directly impact their cost of refinancing. On the other, they’re desperate to maintain market share in a mortgage market that saw transaction volumes shrink during the rate spike.

This explains why Crédit Agricole and other major networks are now offering "excellent" rates around 3.05% for 20-year terms to premium profiles, while advertising 3.56% as their "good" rate tier. The gap between these brackets can cost you nearly €12,000 over two decades on a typical Parisian apartment loan.

What’s driving this generosity? Competition for primo-accédants (first-time buyers) has intensified, with banks offering rates as low as 1.90% over 25 years for qualified buyers purchasing energy-efficient properties. But here’s the catch: these promotional rates serve as bait. Existing customers seeking refinancing rarely qualify for the same terms as new borrowers walking in with fresh applications.

The OAT 10-Year Bond: Your Crystal Ball for Rate Predictions

If you want to predict where French mortgage rates are heading, stop watching talking heads and start monitoring the OAT 10 ans (10-year French government bond). This benchmark currently sits at 3.4%, and its movements directly dictate bank pricing strategies.

When the OAT rises, banks immediately protect their margins by hiking mortgage rates. When it falls, they’re slower to pass savings to consumers. This asymmetry explains why many financial analysts expect rates to stabilize around current levels through 2026, with modest upward pressure possible if inflation persists.

The controversial question dividing French financial forums: will rates drop further, or is this the bottom? The honest answer is that even professional traders can’t say with certainty. What we do know is that the current spread between your existing 4.36% loan and new 3.2% offers is substantial enough to warrant serious analysis, but not so large that waiting automatically constitutes a mistake.

The Real Cost of Renégociation: Beyond the Headline Rate

Here’s where refinancing dreams crash into French banking reality. The advertised rate is just the starting point. You must calculate the TAEG (Taux Annuel Effectif Global), which bundles the nominal rate, mandatory assurance emprunteur (borrower’s insurance), dossier fees, and guarantee costs.

For a €150,000 refinancing, expect to pay:

– Indemnités de remboursement anticipé (early repayment penalties): up to 3% of remaining capital, capped at six months’ interest

– Frais de dossier: €800-1,500 depending on complexity

– New guarantee fees: roughly 1% of loan amount

– Notaire costs: surprisingly, not required for refinancing, but many banks slip in administrative fees that mimic them

One borrower with €100,000 remaining principal should budget at least €1,000 in base fees, with costs scaling up proportionally. If you’re refinancing €300,000, you’re looking at €3,000+ before any savings materialize.

This is why that 0.70% differential matters so much. Below that threshold, the fees can erase five years of modest rate improvements.

Two Paths: Réaménagement vs Rachat de Crédit

French law offers two distinct refinancing routes, and choosing wrong can cost you thousands.

Réaménagement (loan restructuring) keeps you with your current bank. You negotiate modified terms, rate reduction, term extension, or payment suspension. The advantages: lower fees, faster processing, and no new guarantee required. The downside: your bank has zero incentive to offer you their best market rate. They’ll discount your existing loan just enough to keep you from leaving, rarely matching what they’d offer a new customer.

Rachat de crédit (loan refinancing) involves switching banks entirely. The new institution pays off your old loan and issues a new mortgage at competitive rates. This triggers the full fee stack but gives you access to true market pricing. In 2026, with banks aggressively courting new business, this route often yields better rates, even after accounting for higher transaction costs.

The strategic move? Get a competitive rachat offer from a new bank, then use it as leverage for a réaménagement with your current institution. Many borrowers report securing 80% of the savings with 20% of the fees using this approach.

The Energy Efficiency Bonus Nobody Mentions

Here’s a French-specific variable that can tip the scales: your property’s DPE (Energy Performance Certificate). Banks now offer "green" discounts of 0.10% or more for properties rated A or B. If your home qualifies, this bonus can make refinancing profitable even with a smaller rate differential.

Conversely, properties rated F or G face surcharges and stricter lending conditions. Before refinancing, consider whether modest energy renovations could bump your DPE rating and unlock preferential rates. The ROI calculation often favors insulation over refinancing for owners of energy-inefficient properties.

Timing Your Move: The First-Third Rule

The most critical factor in refinancing decisions is where you stand in your loan’s lifecycle. French mortgages front-load interest payments, meaning you pay more interest than principal in the early years. This creates a narrow window of opportunity.

If you’re within the first third of your loan term, refinancing can generate substantial savings. Beyond that point, you’ve already paid most of your interest obligation, and extending the term to reduce payments often increases total cost, even at a lower rate.

For a 25-year loan originated in 2023, that means your refinancing window closes around 2031. Wait too long, and you’re essentially borrowing money to save money, a mathematical dead end.

The Silent Killer: Assurance Emprunteur

While you obsess over basis points, your assurance emprunteur (borrower’s insurance) might be bleeding you dry. This insurance, mandatory for most French mortgages, often costs more than the interest rate differential you’re chasing.

The Loi Lemoine now allows you to switch insurers at any time without penalty. Many borrowers find they can cut their insurance premium by 50% or more by shopping the market. On a €200,000 loan, that’s often €150-200 in monthly savings, far exceeding what rate refinancing delivers.

Before refinancing, optimize your insurance. The savings are immediate, fees are minimal, and you retain the flexibility to refinance later if rates drop further.

Regional Variations: Where You Live Changes the Math

French mortgage rates aren’t uniform. Regional banking competition creates significant spreads. As of February 2026, Normandy averages 3.06% on 15-year loans, while Île-de-France hits 3.12% and Grand Est reaches 3.13%.

This means a Parisian refinancing with a national bank might secure worse terms than someone in Caen using a regional mutual bank. The solution: work with a courtier (mortgage broker) who understands local bank aggressiveness and can pit institutions against each other.

The Market Psychology: Why Waiting Might Be Rational

Current market sentiment is split. Some analysts predict BCE rate cuts could push mortgage rates toward 2.5% by year-end. Others warn that persistent inflation will force rates back above 4%.

The contrarian view: if rates drop further, you’ll refinance again anyway. If they rise, you’ll be glad you locked in today’s rates. This "heads you win, tails you don’t lose badly" logic makes refinancing at a 1%+ differential a reasonable hedge.

But there’s a psychological cost: refinancing requires gathering paperwork, negotiating with banks, and paying fees. Do it twice in two years, and you’ve eroded your savings through transaction costs.

Making the Decision: A Three-Step Test

Before pulling the trigger, run this diagnostic:

-

Calculate your true differential: Compare your current TAEG (not nominal rate) against realistic offers for your profile, not advertised best-case scenarios.

-

Check your loan’s age: If you’re past the halfway point, refinancing rarely makes mathematical sense unless you’re also reducing the term.

-

Model the break-even: Divide total fees by monthly savings. If you won’t own the property long enough to reach break-even, don’t refinance.

A typical 2023 borrower with €180,000 remaining at 4.36% who refinances to 3.2% saves €165 monthly. With €2,500 in total fees, break-even arrives in 15 months. Stay in the home three more years, and you’re €3,440 ahead. Move in one year, and you’ve lost €860.

The Bigger Picture: Debt Strategy Over Rate Chasing

Obsessing over mortgage rates misses the broader point of French wealth management. With inflation running above savings rates, carrying strategic debt can be smarter than rushing to pay it off. The impact of rising interest rates on French mortgage affordability has taught many homeowners that flexibility beats absolute minimization.

Some sophisticated borrowers are even exploring using home equity and debt strategies in France to maintain liquidity rather than chasing marginal rate improvements. Others are using loans against assets as an alternative to traditional financing to avoid refinancing entirely.

Bottom Line: Should You Refinance in 2026?

The answer is a qualified yes, if the numbers work and you act decisively. Rates have dropped enough to create genuine savings opportunities, particularly for borrowers from the 2023-2024 peak. Banks are competing aggressively, and the 0.70% profitability threshold is achievable for many.

But approach with precision. Calculate your TAEG, not just nominal rates. Factor in all fees. Time your application during the first third of your loan. And most importantly, optimize your assurance emprunteur first, it’s often the bigger savings lever.

The refinancing wave is real, but it’s not for everyone. Those who benefit most are organized, mathematically rigorous, and willing to play banks against each other. Everyone else risks spending €1,000 in fees to save €15 a month.

In this market, indecision is the only guaranteed losing strategy. Either refinance now with a clear ROI, or commit to waiting out the cycle. The expensive middle ground is refinancing today, only to watch rates drop further tomorrow while you’re locked into new fees.

Your bank is calling because they need your business. Make sure you need their rate just as badly before you answer.