When a 32-year-old Munich consultant casually mentioned crossing the €300,000 threshold in his investment account, the German financial community did what it does best: it reached for its calculators and skepticism. The claim was simple, nearly everything parked in a single FTSE All-World ETF via Trade Republic. The reaction was predictably German: “Erzähl mal deine Reise. Wann angefangen, Sparrate (savings rate), was geerbt?” (Tell us your journey. When did you start, what’s your savings rate, what did you inherit?)

That comment, echoing the sentiments of many, cuts to the heart of why this story matters. It’s not just about a number. It’s about what that number represents in a country where stock market participation still feels like rebellion against the Sparbuch (savings account) orthodoxy.

The Numbers That Make Germans Uncomfortable

Let’s address the elephant in the room immediately. Reaching €300k by 32 through pure saving and investing requires either time, a high income, or both. Back-of-the-envelope calculations from the community suggest our consultant started investing roughly six years ago with a monthly Sparrate around €3,300. That’s after-tax money flowing directly into his Depot (brokerage account).

For context, entry-level consultants at top-tier firms in Munich (the “Tier 1/2” Unternehmensberatungen) might start at €60-70k brutto (gross), but by senior consultant or manager level, where you’d be after six years, total compensation can easily hit €110-150k all-in. Even after Germany’s substantial taxes and social contributions, that leaves enough room for aggressive saving if you’re disciplined.

The controversial part? Many immediately assumed inheritance played a role. One commenter speculated: “If €230k is invested with only 38% gains, then it’s probably inherited/gifted money.” Another countered with the more optimistic math: a €3,300 monthly investment over six years, compounded with market returns, gets you there. The truth likely sits somewhere in between, perhaps a solid starting salary, consistent saving, and some market tailwinds.

Why the FTSE All-World ETF Became Germany’s Favorite Child

The investment vehicle itself explains part of this strategy’s appeal. The FTSE All-World isn’t just another index tracker, it’s become the default “one-stop shop” for German investors who’ve finally abandoned their Tagesgeldkonto (overnight money account) in search of actual returns.

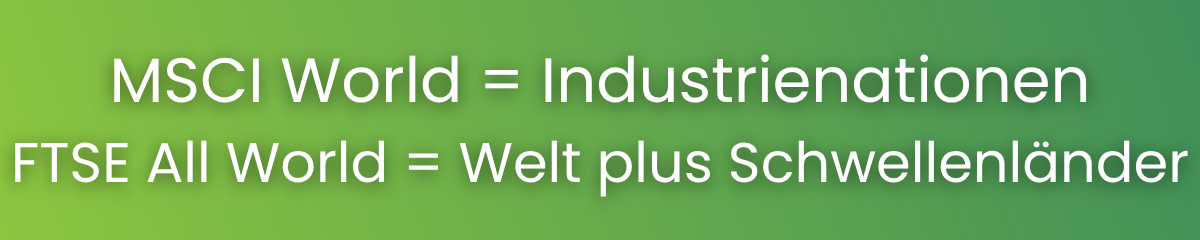

Unlike the older MSCI World, which covers only developed markets (23 industrialized countries, ~1,500 stocks), the FTSE All-World throws in emerging markets too, roughly 4,150 companies across 50+ countries. This means automatic exposure to Chinese tech giants, Indian conglomerates, and Brazilian commodity producers without needing a separate Emerging Markets ETF.

The practical difference shows up in concentration risk. The top 10 holdings in MSCI World represent about 26% of the index. In FTSE All-World, it’s closer to 23%. For a generation that watched Wirecard collapse and Deutsche Bank’s endless troubles, that extra diversification provides psychological comfort.

Trade Republic: The App That Broke German Brokerage

Five years ago, this story wouldn’t have been possible, not because the numbers didn’t work, but because the barriers were too high. Traditional German banks charged €5-10 per trade and treated ETF savings plans as a favor. Then Trade Republic arrived with its “commission-free” model (paid through order flow, but that’s another discussion), making monthly €3,300 investments feasible without bleeding €30 in fees each time.

The platform’s simplicity removed another German finance hurdle: the intimidation factor. No more confusing Kurslisten (price lists) or Telefonorders (phone orders). Just an app, a few taps, and your Sparplan (savings plan) runs automatically. For a consultant billing 60 hours a week, that convenience isn’t trivial, it’s the difference between investing and procrastinating.

The Accumulating vs. Distributing Debate That Divides Germany

Here’s where German tax law turns a simple investment decision into a strategic chess match. Our 32-year-old consultant used an FTSE All-World ETF, but which type? The community didn’t specify, but the choice matters enormously.

Ausschüttender ETFs (distributing) pay dividends quarterly. In Germany, you have a Sparerpauschbetrag (savers’ allowance) of €1,000 per year (€2,000 for married couples). If your ETF yields 2% annually, you can hold up to €50,000 before paying a cent in Abgeltungsteuer (withholding tax). For someone building wealth, this is free money from the Finanzamt (tax office).

Thesaurierender ETFs (accumulating) automatically reinvest dividends. They’re more convenient, no cash drag, pure compound growth, but you largely waste that precious annual allowance. The Vorabpauschale (advance lump-sum taxation) means you still pay some tax, just in a more complicated way.

Many German investors start with distributing ETFs until they exhaust the allowance, then switch to accumulating. At €300k, our consultant has likely outgrown the distributing strategy, his dividends now far exceed €1,000 annually, making the tax difference marginal.

The Inheritance Question: Germany’s Financial Rorschach Test

The immediate assumption that wealth must come from inheritance reveals something profound about German financial psychology. One commenter lashed out: “Typisch deutsches Mindset! Anyone who built something must have inherited. That’s why many don’t even try, because they think it’s only possible with inheritance.”

There’s data behind the skepticism. Germany has one of Europe’s highest inheritance-to-GDP ratios, and wealth inequality is stark. But there’s also truth in the counterargument: this defeatist attitude becomes a self-fulfilling prophecy. When you automatically discount achievement, you remove the incentive to attempt it.

The consultant’s case, working in Unternehmensberatung (management consulting) in Munich, suggests a high but achievable income trajectory. Starting at €65k, reaching €120k+ by 32 is realistic at a good firm. Save 50% of net income, invest consistently, and €300k is mathematically sound, especially with a 38% portfolio gain.

What This Means for Your German Investment Journey

Before you quit reading and open Trade Republic, let’s ground this in reality:

1. The income requirement is non-negotiable. €3,300 monthly savings means earning well above median German income. In 2024, the median full-time salary was €3,975 brutto. Our consultant’s success is inseparable from his career choice.

2. Market timing helped. A 38% gain suggests investing through the post-2020 bull market and recovery. Starting in 2018 would have meant buying dips during COVID. Consistency mattered more than genius.

3. Munich’s cost of living is brutal. Saving that aggressively while paying Münchner Mieten (Munich rents) requires discipline most don’t have. A WG (shared flat) or living outside the city likely helped.

4. The strategy scales poorly. At €300k, a single ETF is fine. At €3 million, you’ll want more sophistication for tax optimization and risk management.

The Bigger Picture: Germany’s ETF Revolution

This story is less about one person’s achievement and more about a generational shift. Young Germans are finally abandoning the Bausparvertrag (building savings contract) and dipping into Aktien (stocks). The numbers prove it: ETF assets in Germany have quadrupled since 2018. Platforms like Trade Republic and Scalable Capital made it possible, low-cost Vanguard and iShares products made it sensible.

The controversy around this €300k milestone shows the friction between old and new Germany. The older generation sees stock market wealth as gambling or inheritance. The younger sees it as necessary survival strategy when Sparbuch interest rates hover near zero and pensions look uncertain.

For those navigating this transition, the path is clearer than ever: choose a low-cost global ETF, automate your Sparplan, max out your Sparerpauschbetrag with a distributing variant initially, and stay consistent. The math works. The controversy is just noise.

Next Steps: If you’re starting your own journey, compare brokers carefully, Trade Republic’s simplicity comes with limitations. Consider whether you need a distributing or accumulating ETF based on your portfolio size. And most importantly, don’t let German skepticism about wealth creation become your excuse for inaction.