You’re earning 64,000 CHF after taxes and saving 24,000 a year. By most standards, you’re winning. Yet the comments tell you to cut that 4800 CHF food budget, 4.40 CHF per meal, and cancel your streaming subscriptions. This is the Swiss financial guilt trip in action: no matter how much you optimize, someone will always point out how you could suffer more.

The real question isn’t whether to save or spend your leftover income. It’s why we’re pretending that 50% of Swiss households can’t save at all because of personal failure, not structural costs.

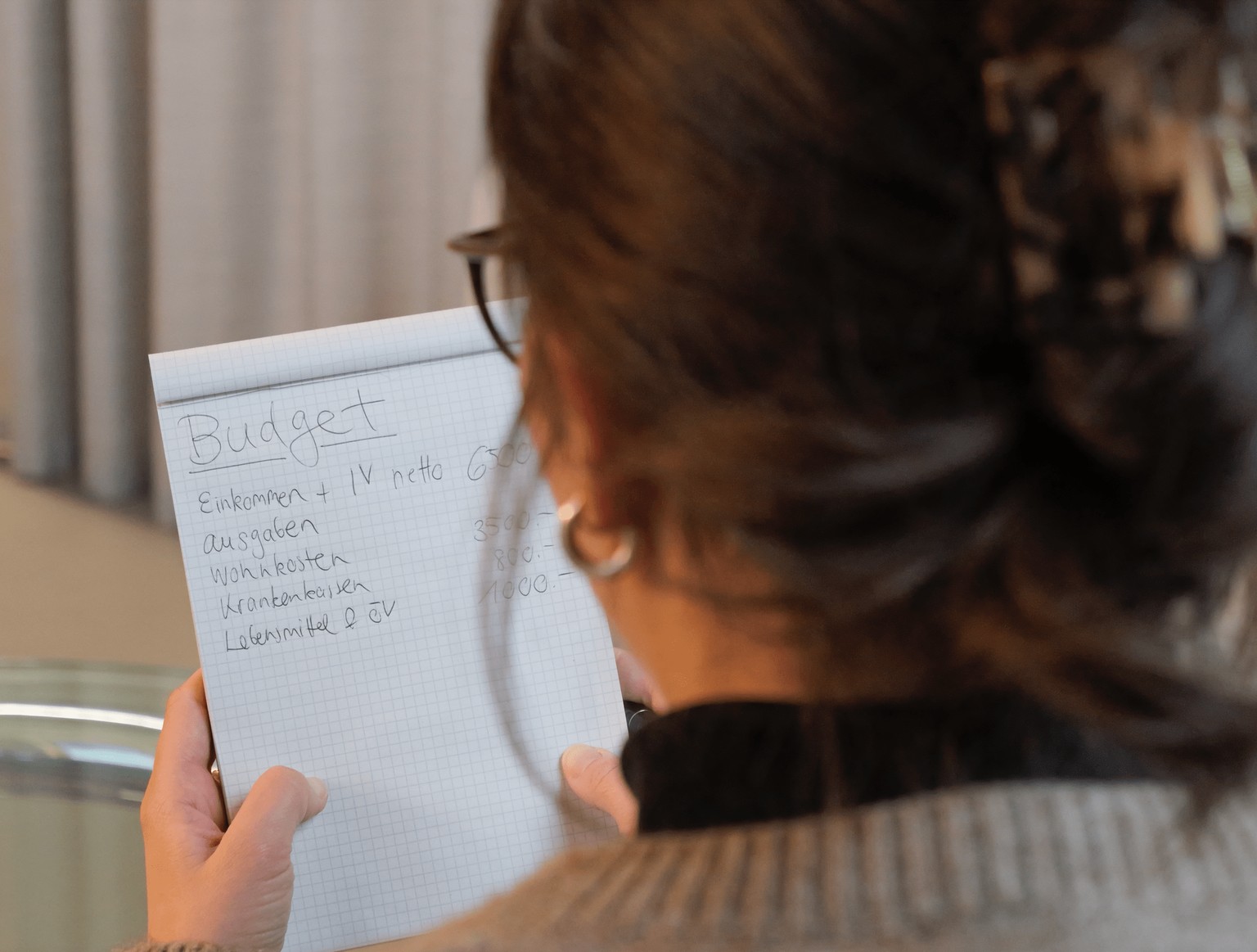

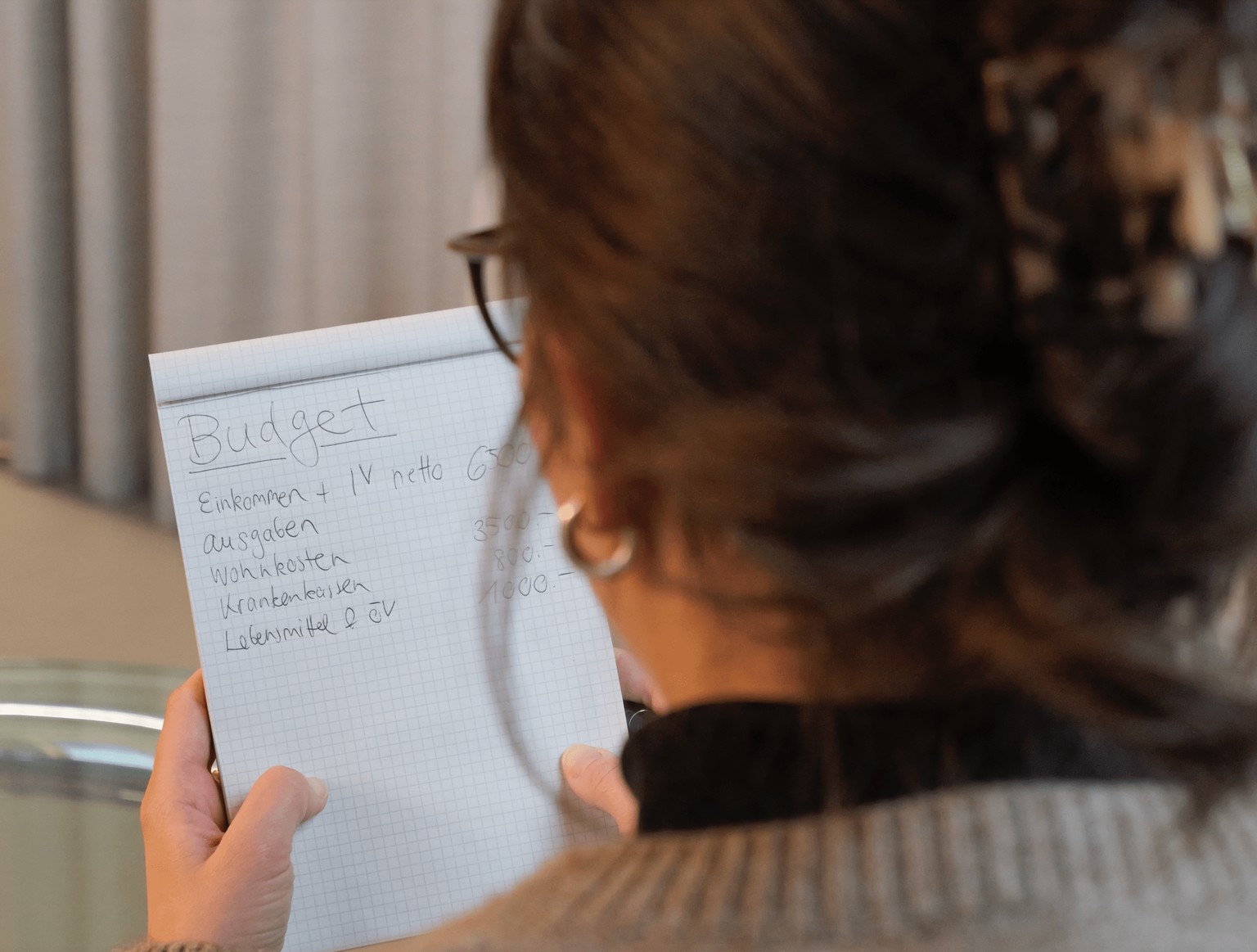

The 3500 CHF Elephant in the Room

Take Melanie, a mid-level tech manager earning the Swiss average of 7200 CHF gross. She lives in her parents’ inherited house with her partner, who receives a partial IV-Rente (Disability Insurance pension) of 300 CHF monthly. Their housing costs alone swallow 3500 CHF, nearly half her income. This isn’t a villa, it’s a standard family home with oil heating, Nebenkosten (additional charges), and wealth taxes that penalize ownership.

The kicker? Her partner’s IV calculation is based on student jobs, not his potential earnings, because his genetic condition manifested post-graduation. The system designed for “financial security” leaves them with zero savings, and the advice they get is “sell the house.” As if that solves the core problem: in Switzerland, housing has become a luxury good that middle-class wages can no longer support.

The “Cook More, Live Less” Fallacy

Back to that 4800 CHF food budget. Commenters called it impressively low, others insisted it was impossible. The truth? It’s achievable if you never buy a sandwich, never grab a pastry, never have a spontaneous meal out. In other words, if you eliminate the small pleasures that make Swiss life bearable during dark February months.

The math is brutal: 4.40 CHF per meal requires planning every single bite, batch-cooking on Sundays, and treating the Migros bakery like a forbidden zone. Sure, you can do it. But should you have to? When your Krankenkasse (health insurance) costs 800 CHF monthly and your AHV/AVS (Old Age and Survivors’ Insurance) contributions keep climbing, the system is already extracting its pound of flesh. Skipping the occasional 12 CHF salad isn’t going to fix your retirement.

When Saving Becomes a Luxury

Melanie’s situation reveals the twisted logic of Swiss financial advice. She spends on “air”, a Ticino trip, a restaurant visit, because her partner is housebound by illness. Cutting these would save maybe 2000 CHF annually, but at what cost? The mental health tax of living in a high-pressure, high-cost society is real, and it’s not deductible.

This is where traditional advice fails. Financial planners love to say “pay yourself first” and “max out your Säule 3a (Third Pillar).” But when 3500 CHF goes to housing and 800 CHF to insurance before you’ve eaten, you’re not choosing between saving and spending. You’re choosing between surviving and slightly less surviving.

The Real Optimization Strategy

If you’re in the privileged position of having leftover income, forget the guilt trips. Here’s what actually works in Switzerland:

- 1. Attack structural costs, not coffee. That 3500 CHF house? Selling and renting a 2000 CHF apartment frees up 1500 CHF monthly, 18,000 CHF annually. That’s not optimization, that’s liberation. The 300 CHF you save by downgrading your mobile plan is noise.

- 2. Consolidate subscriptions intelligently. The Reddit comment about YouTube Premium Family is spot-on: share plans, split costs, but don’t cancel everything. A 15 CHF VPN that lets you access international content is cheaper than a 50 CHF Swiss streaming package.

- 3. Invest the surplus aggressively, once it exists. Many Swiss residents sit on cash, waiting for the “right” moment. If you have an emergency fund and no planned purchases, that money is losing value to inflation. The stock market feels risky, but so does letting 20,000 CHF rot in a PostFinance account earning 0.01%.

- 4. Stop optimizing food to death. If cooking every meal makes you miserable, budget 6000 CHF instead of 4800. The 1200 CHF difference is 100 CHF monthly, less than one therapy session you’ll need from the stress of perfectionism.

The Credit Card Paradox

Melanie uses her credit card for holidays and unexpected costs, a classic Swiss middle-class move. The interest is high, but it’s the only flexible credit many can access. Swiss banks are notoriously stingy with personal loans unless you’re already wealthy.

The better play? Get a 0% interest credit card for 12 months, pay it off religiously, and use it to smooth cash flow. But never carry a balance. That 300 CHF monthly subscription reduction? Throw it at the credit card first. Swiss interest rates will eat you alive faster than a Zurich restaurant bill.

The Bottom Line: Reframe the Question

“Save, invest, or spend?” is the wrong framing. The real question is: “What can I not afford to lose?” For Melanie, it’s her partner’s mental health. For the Reddit budgeter, it’s the flexibility to enjoy Switzerland rather than merely endure it.

The system wants you to feel guilty for not saving enough while it extracts 50% of your income for basics. That’s not a personal finance problem, it’s a policy failure. Your job isn’t to optimize every franc, it’s to secure your foundation, then consciously decide what “enough” looks like.

If that means 24,000 CHF in savings instead of 30,000 so you can ski in Grisons once a year, that’s not failure. That’s understanding that in Switzerland, quality of life has a cost, and sometimes the best investment is in not hating your life.

Actionable framework:

– Month 1-3: Track every franc. Not to judge, but to see where the system is bleeding you (hint: housing, insurance, taxes).

– Month 4: Cut one structural cost. Move, renegotiate insurance, challenge your tax assessment.

– Month 5+: Automate savings to your Säule 3a and emergency fund, then spend the remainder without guilt.

The goal isn’t to retire early on lentils. It’s to live well enough now that you want to stick around for retirement.