Why Your French PEA Is a Tax Trap: Lessons From the $2.2 Trillion Norwegian Fund

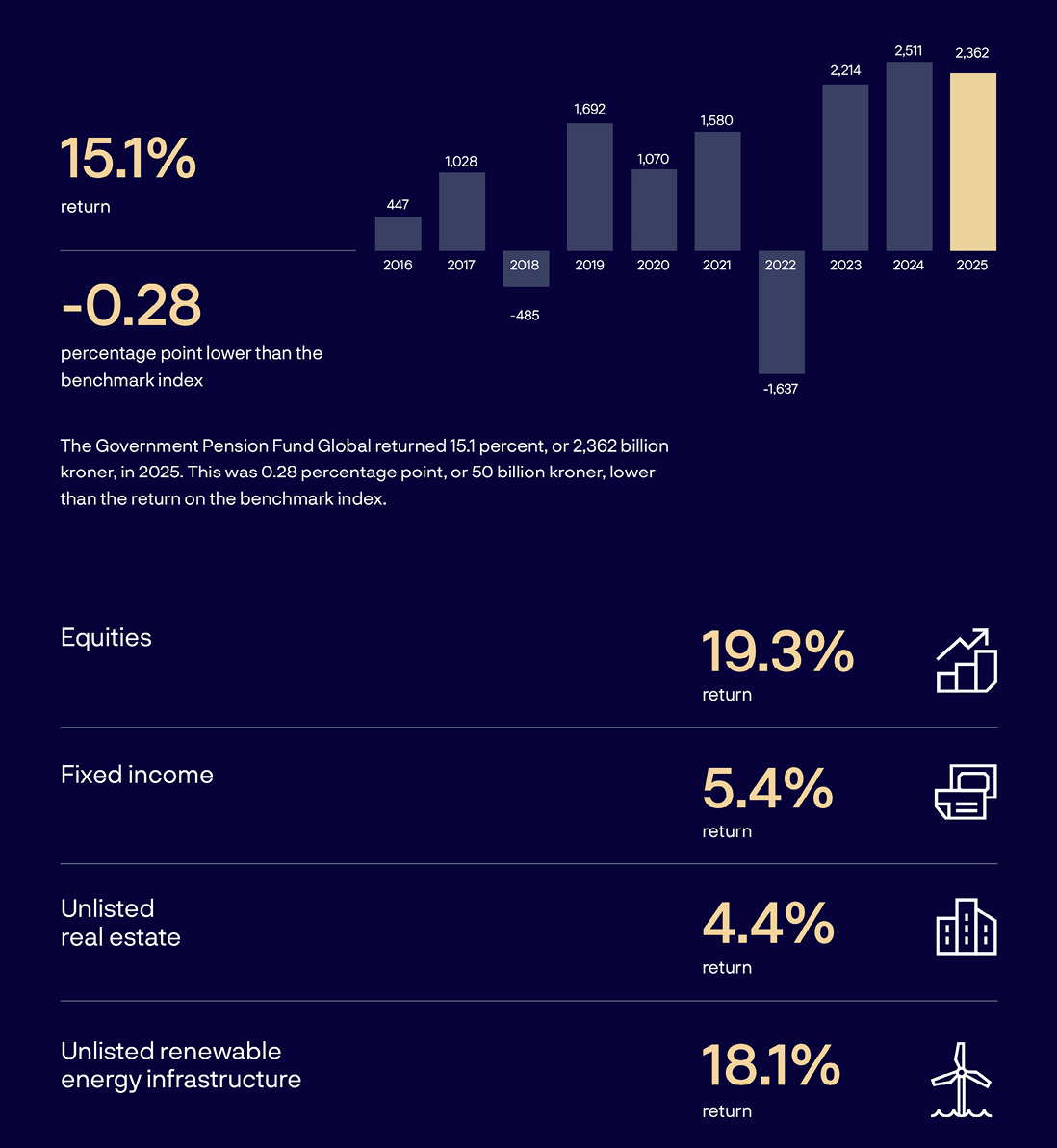

The Norwegian Sovereign Wealth Fund just posted a 15.1% return in 2025, bringing its value to 21,268 billion Norwegian kroner, roughly €1.9 trillion. That performance wasn’t achieved through clever stock picking or market timing. It came from holding 7,201 companies across 68 countries, rebalancing quietly, and paying attention to one thing above all: keeping costs low. For French investors obsessively maxing out their PEA (Plan Épargne Actions) each year, this should be a wake-up call. The tax advantage you’ve been chasing might be costing you more than you think.

The Norwegian Blueprint: Boring Is Beautiful

The fund’s strategy is almost insultingly simple. It holds 71.3% in equities, 26.5% in fixed income, and tiny slivers in real estate and renewable infrastructure. No crypto, no meme stocks, no complex derivatives. The equity portion tracks global indices like the MSCI World, while bonds follow Bloomberg benchmarks. This isn’t passive investing as a philosophy, it’s passive investing as industrial machinery.

What makes this relevant for France? The fund’s edge comes from scale and patience, but the core principles apply to anyone with a brokerage account. The annual report shows management costs at just 0.038% of assets under management. Compare that to the typical French assurance-vie contract, where hidden fees can exceed 2% annually when you factor in fund management charges, arbitration fees, and entry costs. Even a PEA, often celebrated for its tax efficiency, can become expensive if you’re filling it with high-cost ETFs or actively managed French funds.

The Norwegian approach demands you ask: Are you optimizing for taxes or for net returns? In France, these have become confused. The PEA’s promise of tax-free gains after five years has created a cult of the wrapper, where the container matters more than the contents.

The PEA Paradox: When Tax Efficiency Becomes a Cage

French investors poured €192.1 billion into assurance-vie contracts in 2025, with many chasing the PEA’s tax advantages. Yet the Norwegian fund’s results suggest this focus is misplaced. The fund’s 19.3% equity return in 2025 came from global exposure, US tech giants, European financials, Asian chip manufacturers. A typical French PEA investor, constrained by eligibility rules, holds a disproportionate amount of French and European stocks.

The problem? The CAC 40 returned roughly 20% in 2025, but that’s an anomaly. Over the past decade, French large caps have underperformed the MSCI World by significant margins. The Norwegian fund holds just 3.4% of its assets in France, less than its allocation to Japan or the UK. This isn’t anti-French bias, it’s geographic diversification based on market capitalization.

PEA-eligible ETFs exist for global indices, but they often come with higher fees and tracking errors than their non-PEA counterparts. The iShares Core MSCI World UCITS ETF (IE00B4L5Y983) costs 0.20% TER but isn’t PEA-eligible. The PEA-eligible version might cost 0.45% or more, a difference that compounds dramatically over time. Over 20 years, that 0.25% fee difference can cost you tens of thousands of euros on a substantial portfolio.

This is where the Norwegian blueprint becomes subversive. It suggests that for long-term wealth creation, you’re better off using a standard CTO (compte-titres ordinaire) with low-cost global ETFs than a PEA filled with suboptimal products. The tax savings rarely compensate for the performance drag.

The ETF Selection Problem: Quality Over Eligibility

The Norwegian fund uses external managers for specific market segments, but only where they add value. In 2025, it allocated 1,062 billion kroner (about €100 billion) to 103 external organizations, primarily for emerging markets and small-cap exposure. The criteria are strict: managers must demonstrate consistent outperformance after costs.

French investors face the opposite problem. ETF selection often starts with “Is it PEA-eligible?” rather than “Does it track its index efficiently?” The fund’s annual report emphasizes tracking difference, the gap between ETF performance and underlying index, as a critical metric. Many French-domiciled ETFs show persistent underperformance due to poor replication strategies or high collateral costs.

For example, the Lyxor MSCI World UCITS ETF, popular in France, has shown tracking differences of -0.3% to -0.5% annually. That seems small until you realize it’s 2.5 times the Norwegian fund’s total management cost. The Norwegian approach would reject such products outright, regardless of their tax wrapper compatibility.

The solution isn’t abandoning the PEA entirely, it’s being selective. Use the PEA for its intended purpose: direct French and European equity holdings where you have genuine conviction. For global diversification, consider whether the tax advantage outweighs the product quality gap. Often, it doesn’t.

The Fixed Income Illusion: Why Bonds in Your PEA Might Be Pointless

The Norwegian fund holds 26.5% in bonds, but these are global government and corporate securities, not domestic obligations. French investors frequently hold French government bonds (OATs) in their PEA for “stability”, but this creates concentration risk and tax inefficiency.

Bond interest is taxed as income in France, even within a PEA. The wrapper’s advantage only applies to capital gains. This means you’re sacrificing global diversification for a tax benefit that doesn’t fully apply. The Norwegian fund’s bond strategy is purely global, focusing on credit quality and duration across currencies. In 2025, its fixed-income investments returned 5.4%, driven by US and European government bonds, not Norwegian domestic debt.

French investors would be better served holding bonds in an assurance-vie contract, where interest can compound tax-deferred, or in a PER (Plan Épargne Retraite) for retirement-specific goals. The PEA should be reserved for high-growth equity exposure, specifically, individual French stocks where you have specific insights or global ETFs that are genuinely competitive.

ESG and AI: The Norwegian Edge That’s Coming to French ETFs

The Norwegian fund’s 2025 report reveals something surprising: it’s using AI to detect ESG risks at scale. The system scans company reports, news, and regulatory filings to flag controversies before they hit mainstream ratings. This isn’t greenwashing, it’s risk management.

French ETFs are only beginning to integrate such capabilities. Most ESG-labeled products in France rely on third-party ratings that lag market developments. The Norwegian approach suggests that true sustainable investing requires active monitoring, even within a passive framework.

For French investors, this means scrutinizing ESG ETF labels. An ETF that simply excludes tobacco and weapons isn’t applying the Norwegian standard. Look for products that disclose their ESG integration methodology, like the Amundi MSCI World ESG Leaders series. Even better, consider whether ESG matters more than global diversification, the Norwegian fund excludes companies but doesn’t let ESG override its core geographic allocation principles.

The Currency Question: Why Euro Hedging Is Overrated

The Norwegian fund measures performance in a currency basket, not just kroner. In 2025, currency fluctuations reduced returns by 1.155 billion kroner, yet the fund doesn’t hedge systematically. Why? Because currency risk is part of global diversification.

French investors’ obsession with EUR-hedged ETFs misses this point. Hedging costs 0.10% to 0.30% annually and eliminates the natural diversification currencies provide. When the euro weakens, as it did in 2025, unhedged global ETFs deliver higher returns in euro terms. The Norwegian approach accepts currency volatility as the price of true global exposure.

If you’re investing for 10+ years, currency fluctuations tend to balance out. The Norwegian fund’s 6.64% annualized return since 1998 includes significant currency volatility, but the long-term trend remains strong. French investors should question whether EUR hedging is worth the cost, or whether it’s another form of home-country bias disguised as risk management.

Practical Implementation: A French Portfolio Inspired by Norway

Here’s how to apply the Norwegian blueprint within French constraints:

- Core Equity (70% of portfolio):

- 40% in a global equity ETF like the Vanguard FTSE All-World (IE00BK5BQT80) in a CTO

- 20% in PEA-eligible European exposure, focusing on individual stocks where you have conviction

- 10% in emerging markets via a low-cost ETF, possibly in a PER for tax efficiency

- Fixed Income (25%):

- Hold in assurance-vie or PER, not PEA

- Use global bond ETFs or target-date funds that automatically adjust duration

- Consider inflation-linked bonds if you’re near retirement

- Alternatives (5%):

- The Norwegian fund’s 1.7% real estate allocation suggests caution here

- If you must, use SCPI (Sociétés Civiles de Placement Immobilier) within assurance-vie for tax efficiency

The key insight from the Norwegian model isn’t the exact percentages, it’s the discipline. The fund rebalances methodically, doesn’t chase trends, and treats costs as enemy number one. French investors should adopt the same mindset: choose your allocation, stick to it, and optimize relentlessly for fees.

The Controversial Conclusion: Rethink Your PEA Strategy

The Norwegian Sovereign Wealth Fund’s success doesn’t prove that PEAs are useless. It proves that tax wrappers are secondary to investment quality. French savers have been conditioned to prioritize fiscal optimization over global diversification, and it’s costing them.

The fund’s 0.24 percentage point annual outperformance against its benchmark since 1998 came entirely from structural advantages: scale, low costs, and patience. French investors can’t replicate the scale, but they can copy the other two. That means using the cheapest ETFs available, even if they’re not PEA-eligible, and holding them for decades.

The real blueprint isn’t about Norway versus France, it’s about recognizing that in 2026, capital flows globally, and your portfolio should too. The PEA was designed for a different era, when French companies dominated European markets and capital controls were real. Today, it’s often a gilded cage.

Before you make your next PEA contribution, calculate whether the potential tax savings outweigh the certainty of higher fees and home bias. The Norwegian answer is clear: they wouldn’t touch most PEA-eligible products with a ten-foot pole. Maybe you shouldn’t either.

Internal Links for SEO

- For regulatory challenges with ETF strategies: regulatory challenges for ETF strategies

- For French tax-efficient vehicles: French tax-efficient investment vehicles

- For domestic fixed income limitations: limitations of domestic fixed income

- For complex ETF structures: complex ETF structures within tax plans

- For alternative retirement savings: alternative retirement savings instruments