When a government official takes time to address internet rumors about national bankruptcy, you know something unusual is happening. That’s exactly what occurred when Mag. Markus Stix, Managing Director of Markets at Bundesschatz (Austria’s Federal Treasury), personally responded to concerns about Austria’s solvency that were circulating in online finance communities. The response, which he explicitly requested be shared publicly, has sparked more questions than it answered.

The Reddit Rumor That Triggered an Official Response

The controversy began when a poster claimed that holders of Bundesschatzscheine (Federal Treasury Bills) could face expropriation if Austria became insolvent. For Austrian savers who’ve parked billions in these instruments, widely marketed as the safest investment available domestically, this wasn’t just academic speculation. It touched on a fundamental question: is your money truly safe when you lend it to the Austrian state?

What makes the official response remarkable isn’t just its existence, but its content. Stix didn’t simply reassure investors with platitudes. Instead, he delivered a technically precise explanation that reveals both the strength and surprising vulnerabilities of Austrian government debt instruments.

The Technical Truth About Bundesschatzscheine

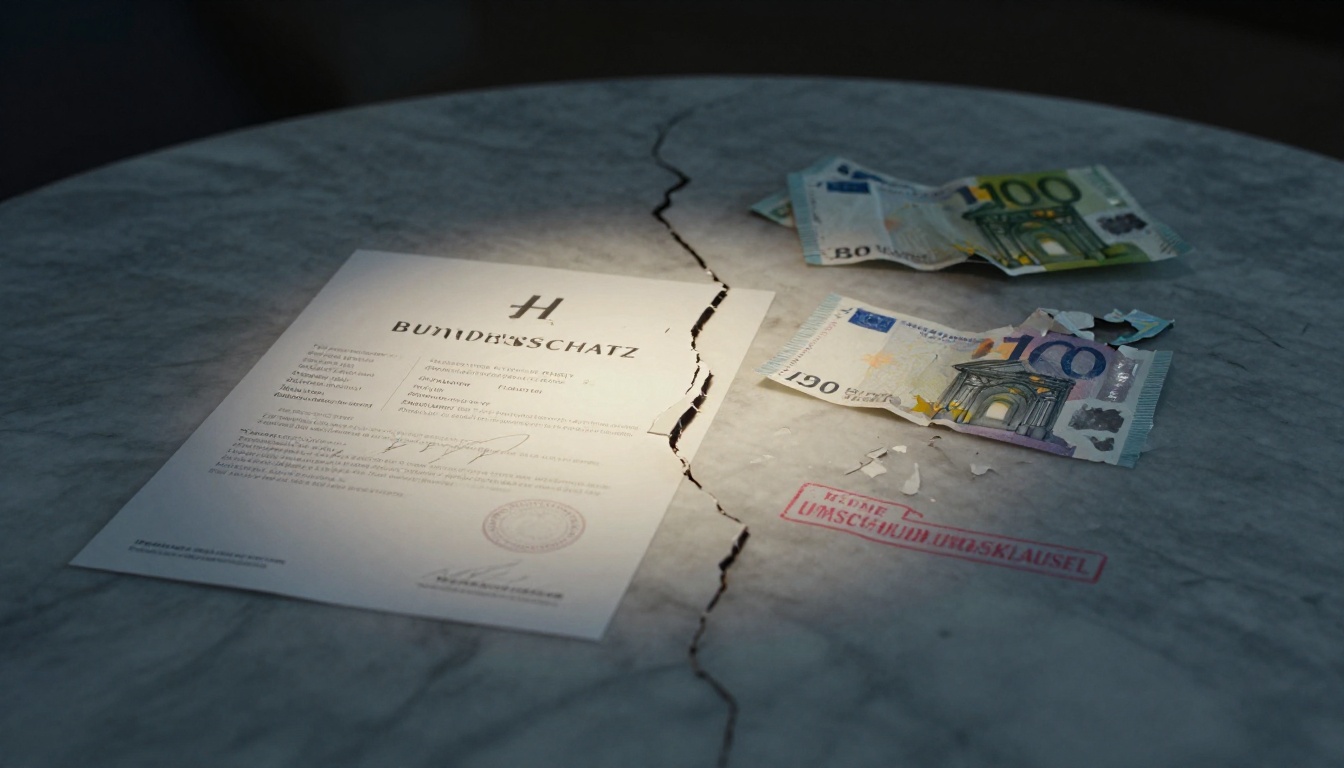

Here’s where it gets interesting. Bundesschatzscheine are not just a brand name, they’re Wertpapiere (securities) of the Republic of Austria, backed by the full faith and credit of the state. In a sovereign insolvency scenario, they would be treated similarly to conventional Austrian government bonds issued under Austrian law.

But there’s a critical difference that should make every Bundesschatz holder pause: Bundesschatzscheine contain no debt restructuring clauses. Unlike Austrian government bonds issued after January 1, 2013, which include Collective Action Clauses allowing orderly restructuring, Bundesschatzscheine are legally naked.

What does this mean in practice? If Austria ever couldn’t pay its bills, bondholders from 2013 onward would have pre-negotiated mechanisms to manage the mess. Bundesschatz holders would be at the mercy of the Austrian Gesetzgeber (legislator), which could pass a law restructuring these debts in any way it saw fit, full repayment, partial forgiveness, or conversion into something else entirely.

As Stix himself wrote: “In the framework of debt restructuring, the Republic of Austria could find practical solutions regarding repayment with Bundesschatz creditors (e.g., full repayment, settlement, partial waiver, debt rescheduling), depending on Austria’s economic performance after insolvency.”

The phrase “depending on economic performance after insolvency” is doing a lot of heavy lifting there. It’s a polite way of saying: you’ll get what you get, and you might not like it.

The Defense Spending Debt Loophole

While the Bundesschatz letter was making waves, Austrian finance officials were busy securing permission to borrow even more. The EU recently activated Austria’s “national escape clause” for defense spending, allowing the government to take on additional debt for Aufrüstung (military buildup) without triggering sanctions.

Finance Minister Markus Marterbauer framed this as merely preserving “budgetary leeway”, emphasizing Austria is “on plan” with its budget. The clause permits up to 1.5% of GDP in additional defense-related debt through 2028, potentially billions in extra borrowing.

Defense Minister Klaudia Tanner welcomed the decision, calling military investments “investments in the security of our country.” She stressed that reaching the 2% GDP NATO target by 2032 requires these higher spending levels.

But here’s the uncomfortable reality: Austria’s current budget deficit already exceeds 4% of GDP, well above the 3% Maastricht limit. The country is under an ongoing EU Defizitverfahren (deficit procedure) requiring deficit reduction. The escape clause doesn’t change these obligations, it just creates a parallel track where defense spending is exempt from the rules everyone else must follow.

Why Ratings Aren’t Reassuring Everyone

Stix correctly noted that Austria maintains high credit ratings: AA+ from S&P, top marks from some agencies, third-best from others. These ratings suggest extremely low default risk. So why the persistent anxiety among investors?

The answer lies in a fundamental disconnect between rating agency methodologies and ground-level fiscal reality. Ratings assess probability of default under current conditions, but they don’t capture the institutional flexibility that makes Austrian debt potentially vulnerable.

Consider the Greek debt crisis. Greek government bonds suffered massive haircuts, yet Greece still exists as a functioning state. Investors who held those bonds lost money, even though the state didn’t disappear. The risk isn’t existential collapse, it’s financial restructuring that leaves creditors holding the bag.

Many international residents monitoring Austria’s fiscal health express similar concerns, noting that while Austria’s ratings remain strong, the trajectory of debt accumulation raises red flags. The combination of persistent deficits, new spending commitments, and legal gaps in investor protection creates a cocktail of uncertainty that ratings alone don’t capture.

This anxiety connects to broader public trust in Austria’s fiscal and social systems. When citizens lose faith in long-term stability, they start questioning even traditionally safe instruments.

What This Means for Austrian Savers and Investors

If you’re holding Bundesschatzscheine, should you panic? Not necessarily, but you should understand what you own.

Bundesschatzscheine remain among the safest investments for Austrian residents, especially for amounts up to the €100,000 Einlagensicherung (deposit insurance) equivalent protection. The probability of Austrian insolvency remains low by any conventional measure.

However, the controversy highlights why savvy Austrian investors are diversifying internationally. Many are exploring Austrian investor behavior and tax-efficient investing strategies that reduce home-country bias. When your own government’s debt instruments have legal loopholes that newer bonds don’t share, geographical diversification isn’t just smart, it’s prudent.

The discussion also reveals why some Austrians are rethinking long-term financial planning strategies. If you can’t trust the “safest” domestic investment to have modern investor protections, how secure is your retirement plan really?

The Political Dimension

The timing of these debates matters. Austria is simultaneously:

– Running deficits above EU limits

– Activating exceptions to borrow more for defense

– Facing questions about debt instrument protections

– Managing public skepticism about fiscal sustainability

This creates a feedback loop. When citizens question debt sustainability, they save more cautiously. When the government borrows more for defense, fiscal hawks get nervous. When official responses highlight legal vulnerabilities, even sophisticated investors start rethinking their allocations.

The defense spending exception is particularly contentious. While Tanner insists it’s “not a blank check”, critics note that labeling spending as “defense” has become a magic wand that makes deficit concerns disappear. One commentator dryly observed that if the Austrian state goes bankrupt, we’ll have bigger problems than lost Bundesschatz investments, like finding a functioning economy.

Practical Takeaways for Your Financial Strategy

1. Understand your instruments: Bundesschatzscheine are simple and safe for small amounts, but they lack the legal protections of modern bonds. For substantial sums, consider diversifying.

2. Watch the deficit trajectory: Austria’s defense spending exemption doesn’t eliminate the need for eventual fiscal consolidation. Monitor whether the government uses the flexibility or abuses it.

3. Diversify geographically: No matter how safe Austrian debt seems, concentration risk is real. International bonds, ETFs, and other assets should complement domestic holdings.

4. Consider credit risk holistically: Austrian banks can demand immediate loan repayment if you lose your job, a risk many don’t realize until it happens. Understanding Austrian credit and loan policies during economic stress helps you prepare for personal financial shocks that might coincide with sovereign stress.

5. Stay informed but rational: The probability of Austrian default remains extremely low. But low probability isn’t zero probability, and the legal structure matters if the unlikely occurs.

The Bottom Line

The Bundesschatz response was both refreshingly transparent and subtly alarming. Refreshing because a senior official directly addressed public concerns. Alarming because it confirmed that Austria’s “safest investment” operates under legal assumptions from a pre-2013 era.

Markus Stix is right that Austrian insolvency is “extremely unlikely.” But as any seasoned investor knows, you don’t prepare for the likely, you prepare for the possible. The controversy isn’t about whether Austria will default tomorrow. It’s about whether the country’s debt instruments provide the same protections investors expect in 2026.

For now, Bundesschatzscheine remain a reasonable place for Austrian residents to park modest savings. But the Reddit discussion that prompted an official response reveals something important: even in stable, wealthy Austria, critical questions about fiscal sustainability and investor protection are no longer confined to academic seminars. They’re being debated in public, and officials are paying attention.

That alone tells you something about how much the landscape has shifted.