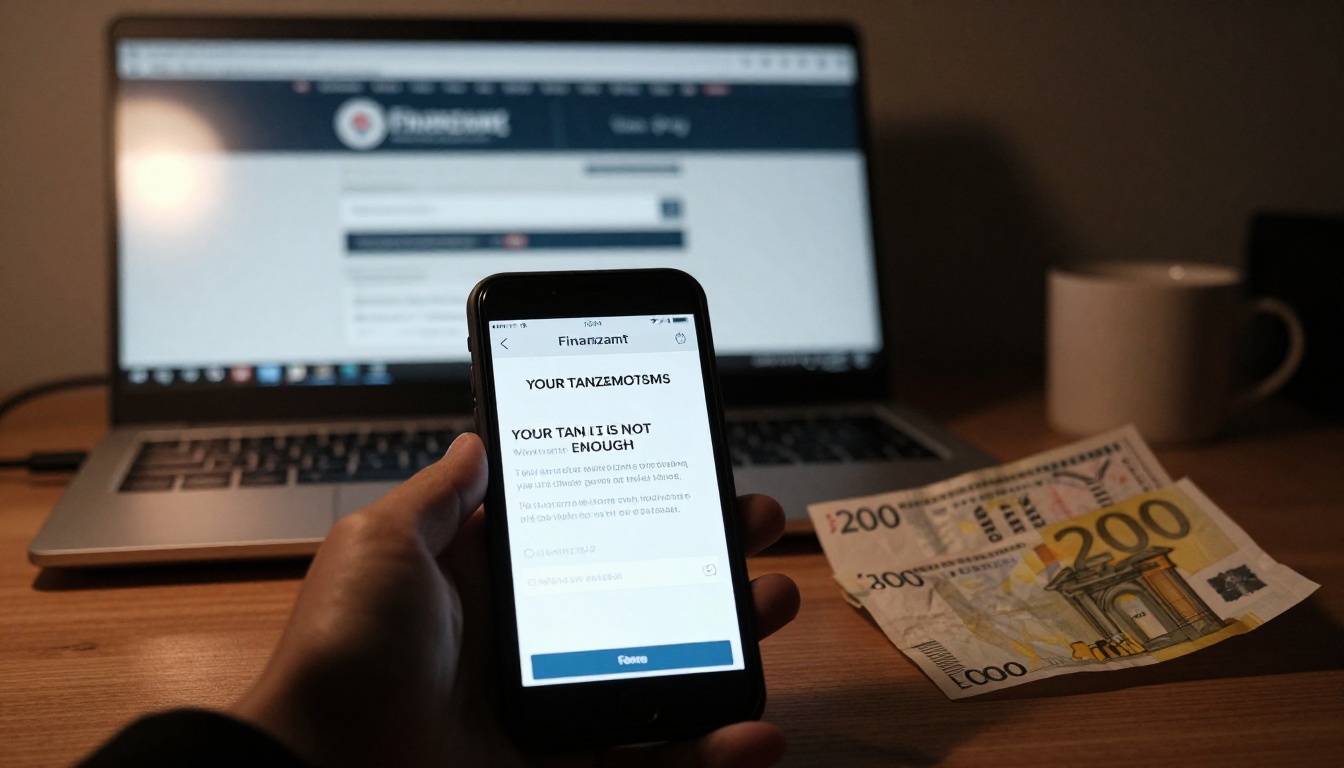

A 70-year-old man from Burgenland registers on what looks like a legitimate investment website. Within days, his life savings, several hundred thousand euros, vanish. Another Austrian, this time from Linz-Land, loses a six-figure sum after receiving an SMS supposedly from the Finanzamt (Tax Office). These aren’t hypothetical scenarios. They’re real cases that happened in Austria in February 2026, and they expose how digital fraud has evolved from crude email scams into sophisticated operations that can empty your account before you even realize something is wrong.

The €200,000 Lesson from an ORF Report

An ORF Bürgeranwalt segment recently highlighted a case where an Austrian lost €200,000 overnight. The details remain partially hidden due to a confidentiality agreement with the bank, but the discussion around it reveals exactly how these crimes unfold. According to analysis from banking security experts, the victim likely received a phishing email that perfectly mimicked their bank’s login page. They entered their credentials, received a push-TAN (transaction authentication number) on their phone, and entered it on the fake site. The criminals then used this authenticated session to make multiple transfers, breaking up the stolen amount into smaller chunks, a technique called structuring or smurfing, to avoid triggering anti-money laundering alerts.

What makes this case particularly instructive is that Austrian banks have multiple security layers. The fraudsters didn’t just need login details, they needed to bypass the Zweite-Faktor-Authentifizierung (two-factor authentication). As one security specialist explained, they likely achieved this by immediately logging into the real banking app with the stolen credentials, which then triggered a push notification. The victim, thinking they were confirming their own login, actually authorized the criminals’ access. Within minutes, the attackers deleted the notification emails from the victim’s inbox, since they often have email access too, and the transfers went through.

Why Austrian Banks Miss the Warning Signs

You might wonder how banks let this happen. Austrian financial institutions have sophisticated fraud detection systems. They flag unusual transactions: payments to new recipients, activity at odd hours, or amounts that deviate from your pattern. Yet these crimes still succeed.

The answer lies in a combination of social engineering and technical gaps. The Linz-Land case shows the classic pattern: first, an SMS phishing message claiming to be from Finanzonline (the Austrian tax portal), then a phone call from someone posing as a bank employee, followed by a fake police officer collecting the victim’s bank card. This multi-stage attack creates a sense of urgency that overrides rational judgment.

Banks face a dilemma. If they delay every suspicious transaction, customers complain about inconvenience. If they let them through, fraud happens. The current system gives banks little room to intervene in real-time. Once you approve a transfer with your TAN, it’s final. This is precisely what the EU’s new PSD3 regulation aims to change.

PSD3: The EU’s Answer to Digital Fraud

Starting in 2028, the Payment Services Directive 3 (PSD3) will fundamentally alter how Austrian banks handle transfers. The most significant change is the mandatory Verification of Payee (VoP). Before any transfer completes, your bank must check if the recipient’s name matches the IBAN. If you think you’re paying “Max Mustermann” but the IBAN belongs to “Kriminelle GmbH”, you’ll get a free warning.

This directly addresses the most common fraud pattern: criminals sending fake invoices or emails with their own IBAN but a trusted name. Austrian banks currently have no obligation to verify this match. Under PSD3, they will.

Another critical change: banks can delay suspicious instant payments. Right now, Sofortüberweisungen (instant transfers) are irreversible within seconds. PSD3 gives banks a time window to block fraudulent transactions. If your bank’s security system flags unusual activity, they can freeze the payment and contact you.

The regulation also shifts liability. Banks that neglect security measures can be held liable for customer losses. This is a major departure from the current situation where customers often bear the loss if they “voluntarily” authorized the payment, even if tricked.

What Austrian Victims Should Do Immediately

If you suspect fraud, speed matters more than anything else. The Polizei (police) and banking experts agree on the immediate steps:

- Call your bank’s emergency hotline, not the regular customer service number. Every Austrian bank has a 24/7 fraud hotline. Find it now and save it in your phone.

- File a police report at your local station or via the Onlinewache (online police station) if your Bundesland (federal state) offers it. In Vienna, you can file digital reports for financial crimes.

- Preserve all evidence: screenshots of the fake website, email headers (not just the visible email address), phone numbers, chat logs. The more data you provide, the better the chance of tracking the criminals.

- Bring your devices to the police. The MeinBezirk report emphasizes this: your phone, tablet, or laptop may contain forensic evidence that helps investigators.

The harsh reality? Recovery rates are low. Criminals typically move funds through multiple accounts within minutes, often crossing borders into non-EU jurisdictions. Austrian police have had success with some cases, but many investigations hit dead ends when funds reach crypto exchanges or offshore accounts.

The Hidden Vulnerabilities in Austrian Banking

Beyond phishing, Austrian residents face other risks. The Reddit discussion touched on a critical point: some Austrian banks still send 2FA activation codes via post. If criminals have your online banking credentials and can intercept your mail, easier than you think in shared apartment buildings or rural areas with unlocked mailboxes, they can activate their own devices.

This vulnerability connects to broader issues with banking privacy vulnerabilities and internal data access risks. While Bankgeheimnis (banking secrecy) protects you from government snooping, it doesn’t protect you from social engineering. Bank employees can see your transaction history, account balances, and personal details. If a criminal poses as you convincingly enough, they might extract information from a helpful call center agent.

Another risk: daily transfer limits. Many Austrian brokerages and banks impose €100,000 daily limits. This becomes problematic when you’re trying to move money for a house purchase or large investment. While it can slow down fraudsters, it also traps legitimate funds. The daily transfer limits locking investors out of their brokerage accounts have become a major frustration for Austrian investors.

How Austrian Fintech Compliance Is Changing

The regulatory landscape is tightening beyond PSD3. Austrian authorities have cracked down on fintech transactions, with Austrian anti-money laundering enforcement impacting routine digital payments. Card Complete, the Austrian issuer behind many credit cards, now demands proof of funds for Revolut top-ups. What seems like a simple transfer triggers AML (Anti-Money Laundering) reviews.

This reflects a broader trend: Austrian fintech compliance and AML checks on digital transactions are becoming increasingly intrusive. A transfer that wouldn’t raise eyebrows in Germany or the Netherlands can trigger a compliance review in Austria. While this aims to prevent fraud and money laundering, it also creates friction for law-abiding customers.

The irony? These strict controls on legal transactions haven’t stopped sophisticated fraud. The criminals behind the €200,000 theft didn’t use fintech workarounds, they exploited traditional banking authentication systems.

Practical Protection for Austrian Account Holders

Given these threats, what actually works?

For individuals:

– Never use SMS for 2FA if you have alternatives. Austrian banks offer app-based authentication (like tanGenerator from Bank Austria or s Identity from Erste Bank). These are harder to intercept than SMS.

– Set up transaction limits. Most Austrian banks let you cap daily transfers. Set this to the lowest amount you can live with. You can always increase it temporarily for large purchases.

– Use a dedicated banking email. Create an email address you use only for banking, never share it, and protect it with a strong password and hardware 2FA if possible.

– Verify independently. If someone calls claiming to be from your bank, hang up and call the official number from your bank card. Don’t use numbers provided in emails or SMS.

For investors with larger sums:

– Split your assets across multiple banks. No single account should hold more than you’re willing to lose in a worst-case scenario. This isn’t just about fraud, it’s also about bank failure, technical outages, or account freezes.

– Understand your brokerage’s withdrawal limits. The brokerage withdrawal limits affecting access to large funds can derail time-sensitive transactions. If you’re planning a large purchase, contact your broker weeks in advance to arrange higher limits.

– Consider a custody solution. For investment portfolios exceeding €100,000, speak with your bank about enhanced security measures. Some Austrian private banks offer segregated accounts with additional authentication requirements.

The Bigger Picture: Trust and Digital Banking

The ORF case ended with a confidentiality agreement, suggesting the bank may have shared liability. This is unusual, typically, banks in Austria deny responsibility if the customer entered a valid TAN, arguing they authorized the transaction. The fact that this case settled indicates the bank may have had security gaps.

This matters because trust is the foundation of banking. Austrian banks built their reputation on stability and security. But as one Reddit commenter noted, “Otto-Normal-Verbraucher ist schlicht und einfach mit der digitalen Welt völlig überfordert” (the average consumer is simply completely overwhelmed by the digital world). The gap between sophisticated fraud techniques and average digital literacy is widening.

The PSD3 regulation, combined with Austrian banks’ own security upgrades, aims to close this gap. But regulations take time. PSD3 won’t be fully implemented until 2028. Until then, your best protection is personal vigilance.

What Happens Next

If you’re reading this because you’ve already been targeted, act immediately. Time is the fraudster’s ally. Every minute you delay gives them another chance to move your money through the financial system, making recovery nearly impossible.

If you’re reading this as prevention, implement the steps above today. Save your bank’s fraud hotline. Set transaction limits. Switch from SMS to app-based authentication. These three actions take less than 30 minutes but could save your life savings.

The Austrian financial landscape is at a turning point. The combination of PSD3, stricter AML enforcement, and evolving bank security will make fraud harder. But criminals adapt quickly. The €200,000 loss case won’t be the last, though with better awareness and faster action, it might be the last time a victim has no chance of recovery.

Your money is only as secure as your weakest security habit. In Austria’s digital banking world, that weakness is often the human element, the tendency to trust, to help, to comply with authority. The fraudsters know this. Your defense is to verify first, trust second, and remember that no legitimate Austrian bank or Finanzamt (Tax Office) will ever rush you into action.