If you’ve ever looked at French salary statistics and thought, “These numbers don’t match my reality”, you’re not imagining things. The official median salary figure plastered across headlines, €2,190 net per month, is technically correct according to INSEE (France’s National Institute of Statistics and Economic Studies). But it’s also a carefully constructed statistical fiction that masks how most French workers actually live.

The gap between what the government reports and what hits your bank account isn’t a rounding error. It’s a €432 monthly chasm that fundamentally warps our understanding of purchasing power, housing affordability, and economic health in France. For anyone budgeting in Paris, negotiating a salary in Lyon, or planning a move to France, this distinction isn’t academic—it’s the difference between financial solvency and a surprise overdraft.

The €432 Illusion: EQTP vs. Reality

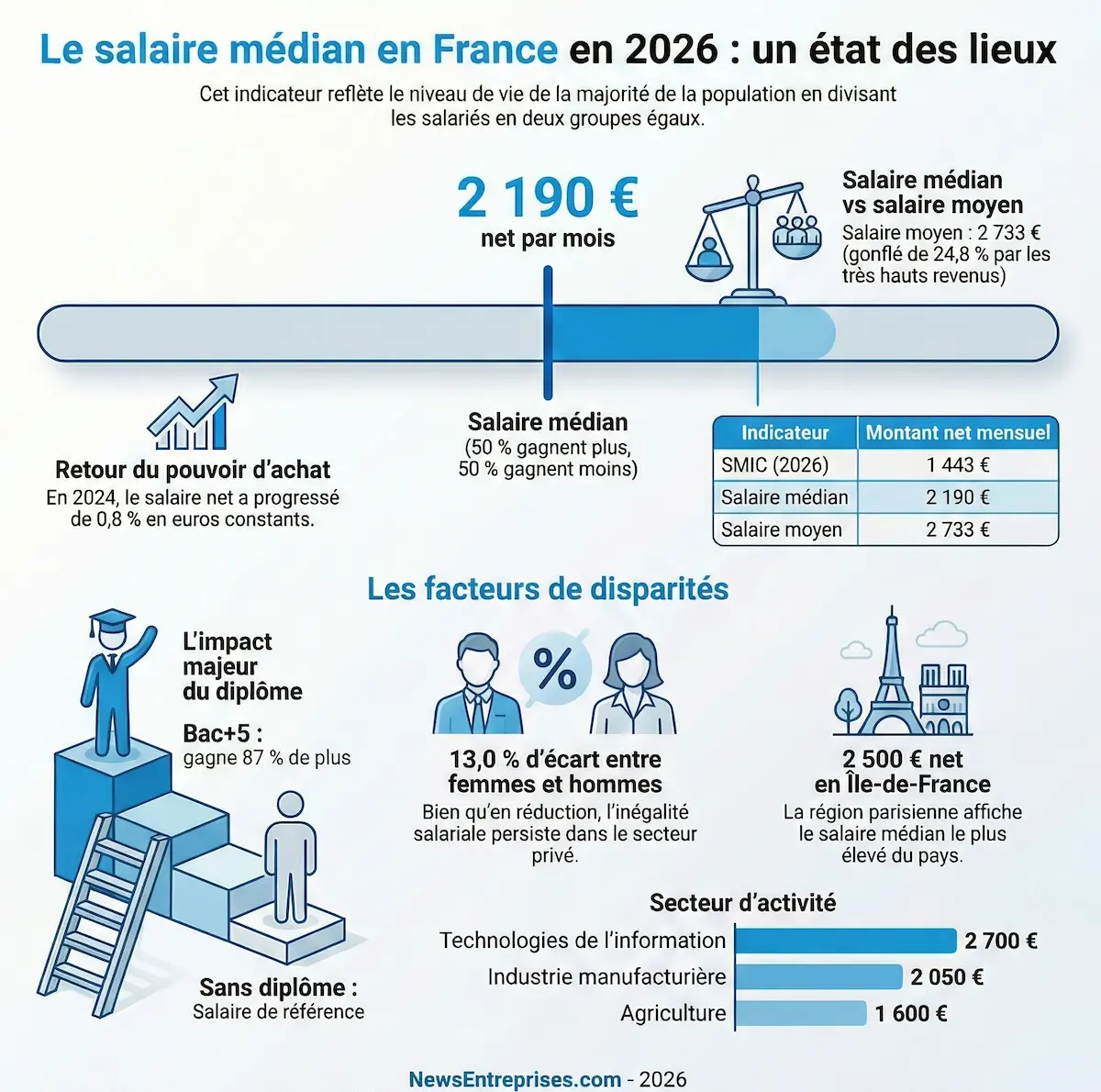

Let’s start with the basics. When INSEE reports the median salary, they use a concept called équivalent temps plein (full-time equivalent or EQTP). This metric standardizes all salaries as if everyone worked full-time, regardless of actual hours. A cashier working 20 hours a week? Her salary gets doubled in the data. A teacher on a 60% contract? Her income appears at 100% for statistical purposes.

The result is a median salary of €2,190 net per month in EQTP terms.

But when the Observatoire des inégalités (Observatory of Inequalities) calculated what workers actually receive, accounting for part-time contracts, seasonal work, and incomplete years, the real median drops to €1,758 net per month.

This isn’t just a technical detail. Half of French employees earn less than €1,758. For employés (clerical workers), the median is just €1,354. For women in the bottom 10%, it’s €238 per month. These are the numbers that determine whether you can cover your rent in Marseille or afford groceries in Lille, not the sanitized EQTP version.

Why Statistics Hide the Truth (And Why They Do It)

The argument for EQTP is straightforward: it allows comparison of hourly wage rates between full-time and part-time workers. A software engineer working 35 hours and another working 17.5 hours can be compared on equal footing. For analyzing wage inequality and gender pay gaps, this makes sense.

But here’s where the logic breaks down: EQTP tells you nothing about actual purchasing power. When you’re paying your taxe foncière (property tax) or renewing your Navigo pass, the bank doesn’t accept a percentage of a full-time salary. You need actual euros.

Many international residents discover this the hard way. They arrive in France, see the €2,190 median, and budget accordingly. Then they land a job at 80% time and wonder why their €1,752 monthly pay doesn’t stretch as far as the statistics suggested. The prélèvement à la source (pay-as-you-earn withholding) system deducts taxes from what you actually earn, not what you’d earn if full-time.

The Part-Time Trap: Not Always a Choice

French labor law makes part-time work seem flexible and worker-friendly. In reality, temps partiel subi (involuntary part-time) plagues sectors like retail, hospitality, and cleaning. A worker might have a 24-hour contract but be scheduled for unpredictable shifts that make a second job impossible. Their EQTP-adjusted salary looks reasonable on paper. Their actual bank balance tells a different story.

Women bear the brunt of this discrepancy. They represent the majority of part-time workers, often due to childcare responsibilities that France’s celebrated but overstretched crèche (daycare) system can’t accommodate. The gender pay gap at full-time is already 13.5%, but when part-time work enters the equation, the real income gap widens dramatically.

A woman working 60% time earns 60% of her male colleague’s pay, but her purchasing power is reduced further by fixed costs that don’t scale down with hours.

This reality check is crucial when demonstrating the disparity between stated earnings and actual housing affordability. A landlord in Paris doesn’t care that your low income is due to part-time work rather than low hourly wages. Their dépôt de garantie (security deposit) and income requirements are based on cold, hard numbers.

The Housing Math That Doesn’t Add Up

Simulation: €1,758 Net Income

- Mortgage: ~€150,000 over 25 years (buys only 3m² in Paris).

- Rent Budget: Max €586/month (Lyon = 15m² studio outskirts; Bordeaux = shared room).

- Reality Check: The €2,190 EQTP figure suggests €730 rent capability, but your pay stub tells the landlord otherwise.

This disconnect helps explain why validating the real purchasing power crisis through household overdraft data shows 24% of French households going into overdraft every month. The tipping point? The 18th of the month, exactly when fixed costs have drained accounts that never matched the rosy statistical picture in the first place.

Financial Planning on Fantasy Numbers

The EQTP illusion creates a cascade of bad financial decisions. Young professionals might accept a 70% contract, thinking €1,500 net is “close enough” to the median. They budget for a normal life, apartment, occasional restaurant, maybe a PEA (Plan d’Épargne en Actions, the French stock savings plan). Then reality hits: after rent, mandatory assurance santé (health insurance top-ups), and transportation, they’re scraping by.

This is particularly damaging for the FIRE movement in France. The Financial Independence, Retire Early crowd often calculates savings rates based on median income statistics. But discussing the illusion of progress and optimizing for poverty on low incomes becomes irrelevant when you realize the baseline numbers are inflated. You can’t save 50% of €2,190 if you only receive €1,400.

Even dollar-cost averaging strategies highlighting wealth-building struggles with limited monthly surpluses become nearly impossible when the surplus is smaller than statistics suggest. The €200 monthly investment that seems reasonable on paper might be half your actual disposable income.

The Political Dimension: Why Governments Love EQTP

There’s a reason why EQTP dominates official communications: it makes the economy look healthier. A higher median salary suggests stronger purchasing power, which justifies policy decisions and paints a picture of prosperity. When the government claims “the median worker earns €2,190”, it implies most people can handle tax increases or reduced benefits. The reality of €1,758 would spark different political calculations.

This statistical smoothing also hides the precarity of contrats courts (short-term contracts) and intérim (temp work). A worker with six months of employment at minimum wage appears in EQTP data as if they earned a full year’s median salary. Their actual annual income might be under €9,000, but the macroeconomic picture looks rosy.

How to Navigate the Data Mirage

So what’s a financially savvy resident to do?

First: Ignore EQTP

Use the real median of €1,758 as your baseline for “typical” income. If you earn more, you’re genuinely above the middle. If you earn less, you’re not failing—the statistics were misleading you.

Second: Negotiate Hourly

When offered a 70% contract, calculate the actual annual income, not the implied full-time equivalent. Ask for the hourly rate and compare it to sector benchmarks, but always translate that into real monthly pay for your specific hours.

Third: Fixed Costs

Factor in costs that don’t scale. Health insurance, transportation passes, and banking fees cost the same regardless of your work percentage. A 50% contract doesn’t mean 50% of a full-time worker’s disposable income—it often means 30%.

Fourth: Context Matters

Use EQTP only for comparing wage discrimination: if your hourly rate is lower than a colleague’s, that’s a problem. But for rent, loans, and lifestyle planning, only real income matters.

The Bottom Line: Demand Real Numbers

The French statistical apparatus isn’t lying, but it is speaking a language designed for economists, not citizens. The €432 gap between EQTP and reality isn’t trivial—it’s the difference between qualifying for a mortgage or not, between financial stability and chronic overdraft.

Next time you see a headline about French salaries, ask: Is this EQTP or real income? Until INSEE and the media routinely publish both figures, workers will continue making life-altering financial decisions based on numbers that describe a parallel universe where everyone works full-time.

Your budget doesn’t live in that universe. Your rent, your groceries, and your compte bancaire (bank account) don’t either. It’s time the statistics caught up to reality.

Key Takeaways

- Real median salary: €1,758 net/month (not the reported €2,190)

- EQTP impact: Inflates incomes by 20% on average

- Affected groups: Women and part-time workers face the biggest disconnect

- Budgeting strategy: Use real income for budgeting, EQTP only for wage comparison

- Housing/Loans: Eligibility depends on actual pay, not statistical equivalents