Your banker smiles, pours you coffee in a glass-walled office, and promises 7% returns on your investment plan. You’re 32, Swiss, with two kids, and this feels like adulthood. But something nags: custody fees, deposit fees, withdrawal fees, and that persistent doubt, does this advice serve your future or the bank’s quarterly targets?

This is where most Swiss residents freeze. The gap between what banks offer and what savvy investors actually do has become a chasm, and the cost of confusion is measured in tens of thousands of francs.

The 7% Mirage: How Bank Fees Devour Your Returns

Let’s dissect that coffee meeting. Your banker proposes two options: upgrade your Pillar 3a (Third Pillar) to an investment plan or open a savings account with investment features. The 7% figure gets tossed out like a fishing lure. What they rarely emphasize is the fee structure that turns that 7% into something closer to 4% net.

Swiss retail banks operate on a simple model: high-touch service funded by high-fee products. Structured investment plans come loaded with front-end fees, annual management charges often exceeding 1.5%, and performance fees that bite whether markets rise or fall. Over 15 years on a CHF 100,000 investment, that 1.5% annual fee compounds into roughly CHF 30,000 in lost wealth, almost a third of your potential gains vaporized.

Many international residents report waiting weeks for banking appointments in major Swiss cities, despite Switzerland’s reputation for efficiency. The irony? That delay costs you nothing compared to the fees you’ll pay for the advice you receive.

Pillar 3a: The Tax-Free Gift You’re Probably Wasting

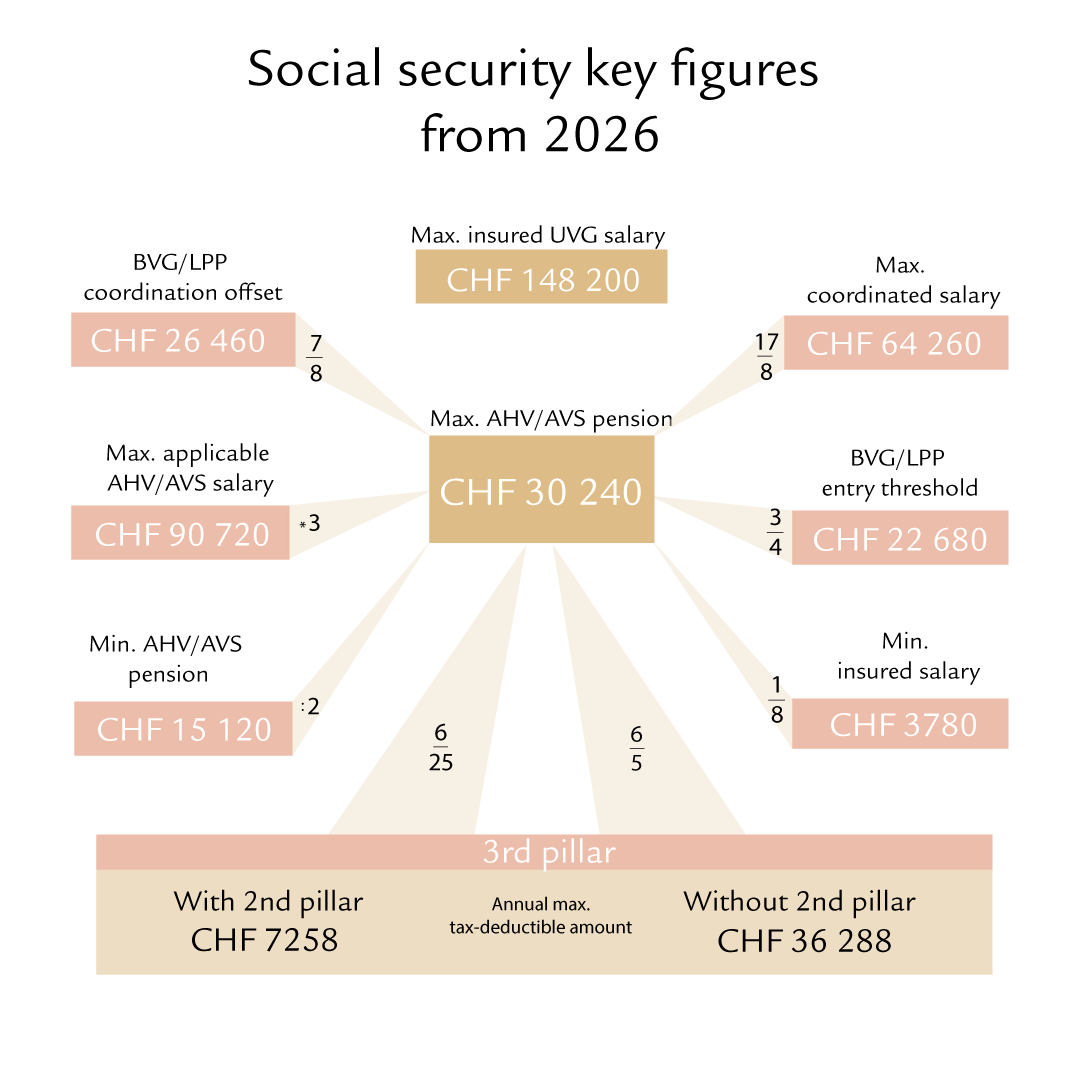

Your standard Pillar 3a earning “basically nothing” is a crime against compound interest. In 2026, you can contribute up to CHF 7,258 annually (or 20% of income up to CHF 36,288 if you’re not in a pension fund). These contributions are fully deductible from taxable income, which immediately saves you CHF 1,500, 4,000 depending on your tax bracket.

But here’s the critical detail: you must invest your 3a, not save it. Traditional bank 3a accounts pay paltry interest, while investment-based 3a solutions through providers like Frankly, VIAC, or finpension let you allocate 95, 99% to global equity ETFs. The difference over decades is staggering.

A new 2026 rule lets you top up missed contributions retroactively for up to ten years. If you’ve left your 3a dormant, this is your chance to catch up, but only after you’ve maxed out the current year’s ordinary contribution. This matters because letting your 3a grow too large (above CHF 40, 50k) before opening a new one can create tax inefficiencies later when you withdraw.

The ETF Escape Route: Why Interactive Brokers Isn’t the Boogeyman

The alternative whispered across Swiss personal finance circles is simple: open an account with Interactive Brokers (IBKR) and buy one or two broad ETFs like VT (Vanguard Total World Stock ETF) or VOO (S&P 500). The total expense ratio? Around 0.07% annually. That’s 20 times cheaper than typical bank products.

Yes, the platform looks intimidating. Yes, you’ll need to execute trades yourself. But the security concerns are largely misplaced. When you buy ETFs through IBKR, those securities are held in custody under your name. If IBKR Switzerland were to go bankrupt, a highly unlikely scenario given FINMA regulation, your ETFs remain your property, not part of the bankruptcy estate. The legal framework in Switzerland, governed by the Finanzmarktinfrastrukturgesetz (Financial Market Infrastructure Act), mandates strict separation between broker assets and client securities.

Market Crashes: The Fear That Costs You Everything

“If I invest CHF 100,000 over 15 years and there’s a market crash, what happens?” This question reveals the fundamental misunderstanding banks exploit. A crash reduces the value of your holdings temporarily, whether they’re in a bank’s structured product or a low-cost ETF. The difference is recovery.

Historical data shows every decade has at least one major crash: 2000 (, 45%), 2008 (, 55%), 2020 (, 34%), 2022 (, 20%). Each time, broad market indices recovered and reached new highs. A CHF 10,000 investment in the MSCI World in 2005 grew to roughly CHF 38,000 despite these catastrophes. The same amount in a savings account? CHF 12,200.

The key is never investing money you’ll need within five years. Your emergency fund, six months of expenses, typically CHF 15,000, 25,000, belongs in a savings account, not the market. Everything else should be working for you.

Tax Reporting: The Myth vs. Reality

Swiss residents fear that investing through foreign brokers turns their Steuererklärung (tax declaration) into a nightmare. The reality is more mundane. IBKR provides an annual tax report detailing dividends, interest, and portfolio value. You list each holding in your tax software, more holdings mean more lines, but not more complexity.

Swiss capital gains are tax-free for private investors, a massive advantage over Germany or France where you’d pay 25, 40%. You do pay income tax on dividends and wealth tax on your total assets, but these apply regardless of broker. The 35% withholding tax (Verrechnungssteuer) on Swiss dividends gets refunded when you declare everything correctly.

For most cantons, the process takes an extra 30 minutes annually. That’s a small price compared to paying CHF 2,000+ in unnecessary bank fees every year.

The Real Cost of Waiting

Every year you delay investing costs you real money. If you invest CHF 500 monthly at a realistic 6% return, waiting just one year reduces your final wealth after 30 years by over CHF 16,000. Waiting five years? You lose CHF 85,000.

The Swiss investment landscape has evolved beyond traditional banks. Neobanks like Neon offer fee-free ETF purchases for select funds. Robo-advisors provide automated portfolios at 0.5, 0.7% annually, still more expensive than DIY but far cheaper than bank products. The rise of these alternatives reflects a simple truth: investors are waking up to the fee drain.

Your 4-Week Escape Plan

Week 1: Audit Your Finances

Pay off consumer debt. Build your emergency fund. Calculate how much you can invest monthly. Even CHF 100 is a start. If you have CHF 15,000 sitting idle, practical first steps for new investors with modest capital can guide your initial moves.

Week 2: Fix Your 3a

Open an account with Frankly, VIAC, or finpension. Set a standing order for CHF 605/month (maxing the CHF 7,258 annual limit). Choose an equity allocation of 80, 100% if you’re under 45. This step alone saves you thousands in taxes annually.

Week 3: Start Free Investing

Open an IBKR account. Buy one global ETF like VT or a combination of VOO and a Swiss index. Set up a monthly savings plan. Don’t overthink it, evolving investment strategies beyond simple ‘set-and-forget’ portfolios shows that even sophisticated investors start simple.

Week 4: Automate and Ignore

Let the standing orders run. Check your portfolio quarterly, not daily. Your job is to be patient, not active. The biggest wealth destroyer is panic-selling during drops.

The Bottom Line

The Swiss banking system operates with the same reliability as an SBB train, usually impeccable, until construction slows the line. Right now, the construction is the fee structure that banks refuse to dismantle. You can wait for the line to clear, or you can switch to the express route that’s been there all along.

The 7% promise costs you 30% in fees. The DIY route costs you 30 minutes of learning and saves you a small fortune. Your kids’ education, your retirement, your financial peace of mind, these are too valuable to fund your banker’s bonus.

Start today. Open that 3a. Buy that first ETF. The confusion is intentional, the solution is simple.