Morningstar just dropped its European Active/Passive Barometer 2025, and the numbers are sobering. Only 11.4% of European active equity funds managed to beat their passive counterparts over a decade. That means nearly nine out of ten professional fund managers, people paid handsome salaries to outperform, failed to do the one job they were hired for. The report covers roughly 32,000 funds domiciled in Europe, representing about half the market’s assets, so this isn’t a fluke statistic from a small sample.

The Methodology That Exposes Active Management’s Weakness

What makes Morningstar’s analysis particularly brutal is its methodology. Unlike simplistic comparisons that pit active funds against theoretical indexes, Morningstar compares them against real passive funds that actual investors can buy. This means the benchmark includes the real-world costs of passive investing, fund fees, transaction costs, and tracking errors. The active funds aren’t losing to an academic ideal, they’re losing to the humble ETF sitting in your PEA (stock savings plan).

The barometer also evaluates funds based on their starting category, simulating the real choices an investor would have faced years ago. And it measures performance on a euro-weighted basis, meaning larger funds count more heavily. This approach eliminates the most common criticisms of active/passive studies. You can’t dismiss these results by claiming survivorship bias or unrealistic benchmarks.

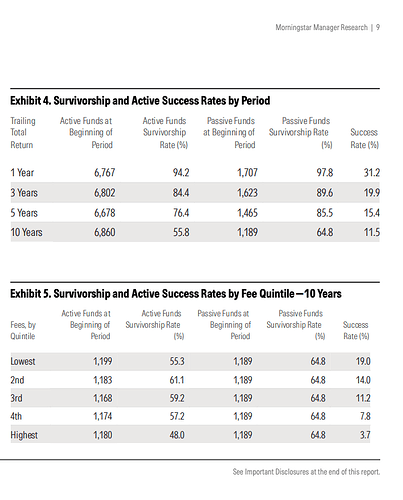

Speaking of survivorship, 44% of the active funds that existed ten years ago have since merged or closed. If you invested in one of those funds, you didn’t just underperform, you likely faced a forced exit at an inconvenient time.

The Fee Factor: Where Active Management Goes to Die

Here’s where the story gets expensive for investors. Morningstar cross-referenced performance with fee levels over ten years. In the cheapest quintile of active funds, 19% managed to beat their passive equivalents. In the most expensive quintile? A dismal 3.7% success rate.

The math is stark. Traditional active funds charge an average of 1.32% in management fees, according to Le Point’s analysis. Active ETFs, a newer hybrid category, charge around 0.37%. Pure passive ETFs average just 0.27%. That one percentage point difference might sound trivial, but compounded over a decade, it devours returns.

Many French investors don’t realize how fee structures work in their assurance-vie (life insurance) contracts or comptes-titres (securities accounts). Banks often layer fund fees on top of their own management fees, creating a double drag that makes the 1.32% average look optimistic. When your active fund needs to outperform by 1.5% annually just to break even with a passive alternative, you’re fighting arithmetic itself.

The Short-Term Illusion vs. Long-Term Reality

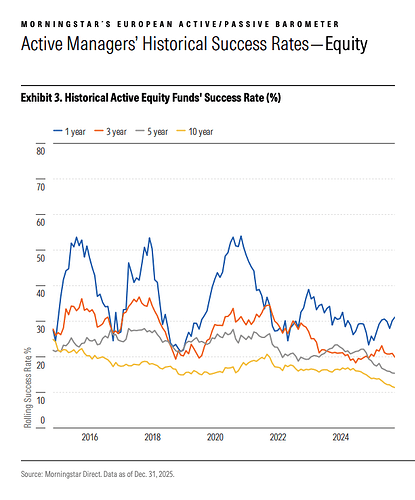

Active funds look better over shorter periods, which helps explain why they still attract capital. Over one year, 31.2% outperform, basically a coin flip. At three years, it’s 19.9%. At five years, 15.4%. The longer the timeframe, the more the odds tilt against active management.

This pattern creates a psychological trap. Investors see an active fund beat the market for a year or two, assume skill is involved, and pile in. By year six or seven, the outperformance has evaporated, but the high fees remain. The fund quietly merges into another product, and the cycle repeats.

Many forum discussions reveal this pattern among French investors. The sentiment is clear: after trying multiple active funds through their bank’s conseiller en gestion de patrimoine (wealth management advisor), they’ve seen the same story play out. Strong initial performance, followed by regression to the mean and disappointing net returns.

The Risk Management Defense: A Valid Counterpoint?

Not all active funds aim to maximize returns. Some target improved risk-adjusted performance, better Sharpe ratios, lower volatility, smaller drawdowns. As one experienced investor noted, certain strategies are optimized to protect capital rather than chase returns. In market downturns, these funds might lose less, even if they gain less during rallies.

This is a legitimate strategy, but it raises a question: are you paying 1.32% annually for downside protection you could achieve through simpler means? A well-constructed portfolio of passive ETFs with appropriate bond allocations and maybe some gold can provide similar risk management at a fraction of the cost.

The data suggests most investors would be better off with a passive core and a small allocation to alternative strategies, rather than betting their entire portfolio on an active manager’s ability to time markets or pick winners.

The French Context: PEA and Regulatory Complications

For French investors, the active vs passive debate has additional layers. The PEA offers significant tax advantages, exemption from capital gains tax after five years, but restricts eligible investments to European securities. This has created a thriving market for European equity ETFs specifically designed for PEA compliance.

However, regulatory threats loom. Rumors have circulated about potential restrictions on non-French ETFs within the PEA, which could limit access to the best passive options. Our coverage of the regulatory threats to passive ETFs in France shows how political considerations can interfere with rational investment choices.

Meanwhile, French banks continue to push active funds through their services de gestion sous mandat (managed account services). As we exposed in our investigation of conflicts of interest in active fund management, some institutions have remuneration structures that encourage portfolio churning, buying and selling securities to generate transaction fees. This directly harms returns and makes passive strategies even more attractive by comparison.

The Rise of Active ETFs: A Hybrid Solution?

The market is evolving. Active ETFs, funds that use active strategies but trade like passive ETFs, have exploded in Europe, doubling to over €77 billion in a year. They represent 3% of the European ETF market but capture 7% of flows. In the US, there are now more active ETFs than passive ones.

The pitch is compelling: active strategies with ETF liquidity and lower fees (0.37% vs 1.32%). But here’s the catch: Morningstar’s data shows that even at lower fee levels, most active strategies still underperform. The fee reduction helps, but it doesn’t solve the core problem, identifying in advance which managers will outperform.

Major players like J.P. Morgan, Fidelity, and Pimco dominate this space. French investors can access these through their brokerage accounts, but they should ask: am I paying a premium for the idea of active management, or for actual, persistent skill?

What About Individual Stock Picking?

The active vs passive debate often conflates professional fund management with individual stock picking. Some argue these are entirely different games. Professional funds face massive constraints: size limits, redemption pressures, benchmarking requirements, and career risk that forces herding behavior.

An individual investor with a small portfolio can take concentrated positions, hold through volatility, and ignore quarterly performance pressures. This flexibility theoretically allows for higher returns, albeit with higher risk.

The statistics on individual stock pickers are less clear than for professional funds, but the consensus among serious investors is sobering. Most individuals underperform, and those who succeed often do so through luck rather than skill. As one forum commenter pointed out, while stock picking has a place in a portfolio for volatility exposure, treating it as your primary strategy is statistically unwise.

If you’re determined to pick stocks, limit it to a small portion of your portfolio, maybe 5-10%, and treat it as educational entertainment rather than a retirement plan. The data is overwhelming: for the core of your wealth, passive is the rational choice.

Practical Takeaways for French Investors

So what should you actually do with this information?

First, build your core portfolio with low-cost, diversified passive ETFs. If you’re using a PEA, focus on European equity ETFs that qualify for the tax advantages. For global exposure, consider an assurance-vie with access to international passive funds, the tax treatment is different but still favorable.

Second, watch fees like a hawk. Whether in a PEA, assurance-vie, or CTO (compte-titres ordinaire, standard securities account), total fees above 0.5% annually need justification. Many French bank-sold products charge 1.5-2% when you include all layers, unacceptable in the age of cheap ETFs.

Third, resist the temptation to chase past performance. That active fund that outperformed last year has a 70% chance of underperforming over the next five years. The statistics are brutal and consistent.

Fourth, if you must have active exposure, consider active ETFs rather than traditional funds. The fee savings matter, and the liquidity is useful. But keep the allocation small, maybe 10-20% of your equity position.

Fifth, understand that trying to time the market is even harder than picking winning funds. The combination of market timing and active management is a recipe for disappointment.

The Bottom Line

Morningstar’s 2025 barometer isn’t just another data point, it’s a comprehensive indictment of the active management industry in Europe. The 11.4% success rate over ten years, combined with the 44% fund mortality rate and the fee drag, creates a compelling case for passive investing.

Yet the debate persists because hope is more compelling than data. Every investor believes they can identify the next great manager, the next winning strategy. The financial industry thrives on this optimism, selling expensive products with compelling narratives.

For French investors navigating the complexities of the PEA, assurance-vie, and bank-sold products, the path forward is clear: keep costs low, stay diversified, and treat active management as a small satellite rather than a core holding. The data doesn’t lie, even if the marketing does.

The active management industry won’t disappear, it will evolve, as we’re seeing with the rise of active ETFs and thematic strategies like the rise of values-based passive funds. But for building long-term wealth, the humble passive ETF remains your most reliable ally.