You finally decided to invest €10,000 in an actively managed European equity fund. The markets cooperate, your fund gains 2% over the year. Pop the champagne? Not so fast. That €200 profit never reaches your account. Instead, it vanishes into a complex fee structure where your bank, wealth advisor, or financial intermediary pockets nearly half.

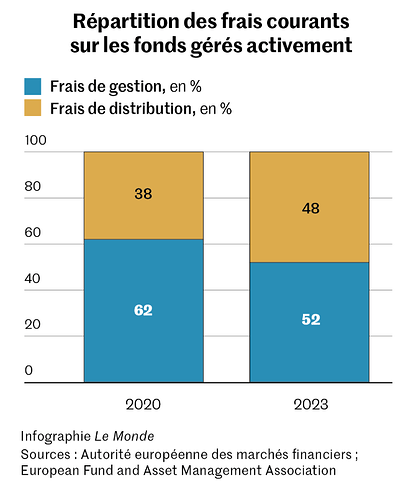

This isn’t a hypothetical. According to a recent ESMA (European Securities and Markets Authority) report from November 2025, fund distributors across Europe now capture 48% of all ongoing charges in actively managed funds, up from 38% just three years prior. For the first time, the middlemen are taking as much as the actual fund managers who research, select, and monitor your investments.

The Retrocession Riddle: How Banks Get Paid Twice

The mechanism behind this fee grab is called rétrocessions (retrocessions), commissions that fund managers secretly kick back to the distributors who sell their products. These aren’t transparent line items on your statement. They’re buried in the total expense ratio, representing a staggering 45% of all ongoing costs, yet remaining invisible to the average investor.

Here’s how the French version plays out: You walk into your local BNP Paribas or Société Générale branch. The conseiller (advisor) recommends a “high-performing” actively managed fund. What they don’t mention is that for every euro you pay in management fees, roughly half flows back to the bank, not for managing your money, but for having successfully sold you the product.

Many international residents report waiting weeks for banking appointments in Paris, despite expectations of streamlined processes. When they finally sit down, they’re often presented with complex products where the fee structure remains deliberately opaque. This creates a system where conflicts of interest in French bank remuneration models leading to excessive trading become almost inevitable.

The Transparency Mirage: Why You Can’t See What You Pay

French regulators require a DICI (Document d’information clé pour l’investisseur, or Key Investor Information Document), but these documents often obscure more than they reveal. The retrocession amounts appear as aggregated figures, if at all. You might see a total ongoing charge of 2.2% per year, but nowhere does it clearly state that 1% goes to your bank simply for the initial sale.

This opacity extends beyond mutual funds. French investors face similar challenges with complexity and lack of transparency in structured products sold through assurance-vie, where €42 billion flowed into instruments most purchasers cannot explain. The same pattern appears in hidden costs and sustainability of high returns in euro funds within assurance-vie, where the mechanics of achieving “guaranteed” returns remain deliberately vague.

The Real Cost: When Fees Devour Returns

Let’s translate this into real numbers. That €10,000 investment gaining 2% annually sees its entire profit consumed by fees. Over five years, assuming the same performance, you’ve paid roughly €1,100 in total costs, with €528 going to intermediaries who’ve done nothing beyond the initial sale.

But the damage compounds. While you’re earning zero real returns after fees, the CGP (conseiller en gestion de patrimoine, or wealth advisor) continues receiving their retrocession year after year. This creates a perverse incentive: the advisor gets paid ongoing commissions regardless of performance, while you bear all the market risk.

The situation mirrors broader concerns about opaque and rising bank fees eroding retail investor returns, where simple account maintenance has evolved into a significant annual expense.

The International Rebuke: What France Refuses to Learn

The United Kingdom and Netherlands banned retrocessions in 2014. The results? Lower overall fees and improved quality of financial advice. Without the crutch of hidden commissions, advisors had to demonstrate actual value to earn their keep.

France, meanwhile, remains stubbornly attached to the status quo. Banks and wealth management firms, heavily dependent on this revenue stream, have successfully resisted reform. The AMF (Autorité des marchés financiers, France’s financial markets regulator) did sanction three asset management companies in 2025 over retrocession practices, but this amounts to wrist-slapping in a system that requires structural change.

This resistance becomes even more striking when considering how banks profit from government bond transactions through opaque fees. Many investors assume buying obligations d’État (government bonds) should be straightforward, after all, you’re lending directly to the French state, yet banks layer fees onto products that need no active management.

The Generational Tipping Point

Here’s where the math gets interesting for France’s financial future. The current generation of investors, many approaching retirement, accepted these fee structures as normal. Their heirs, however, show no such loyalty.

Younger French investors, armed with comparison tools and comfortable with digital platforms, increasingly ask a simple question: “Why should I pay 3% in total fees for a fund that underperforms a low-cost ETF?” This skepticism extends to real estate investments, where SCPI liquidity issues and structural fee opacity in French investment products have revealed that supposedly “safe” real estate can become a trap when redemption requests exceed available cash.

The Clean Share Alternative: A Path Forward

Some independent advisors are pioneering a better model. Instead of selling high-fee active funds with fat retrocessions, they recommend clean shares, essentially low-cost ETFs and index funds without hidden commissions. They then charge transparent advisory fees based on assets under management.

Consider the math: A traditional active fund charging 2% total fees (with 1% retrocession) might deliver market performance minus 2% annually. Switch to an ETF costing 0.20% plus a 1% transparent advisory fee, and your net performance improves by 0.80% per year. Over decades, this difference amounts to tens of thousands of euros.

This transparency-focused approach aligns advisor incentives with client success. When advisors charge explicit fees for service rather than hidden commissions for sales, they must demonstrate ongoing value. This model also facilitates better fiscal transparency and comparative performance of investment wrappers like assurance-vie, where open-source simulations have exposed the true costs of different investment structures.

Your Action Plan: Cutting Through the Fee Fog

If you’re investing in France, here’s how to protect yourself:

1. Demand Fee Decomposition: Ask your advisor to explicitly separate management fees from distribution fees. If they can’t or won’t, that’s your answer.

2. Question Active Management: For most investors, low-cost ETFs through a PEA (Plan d’épargne en actions, or equity savings plan) or CTO (compte-titres ordinaire, or standard securities account) outperform expensive active funds after fees.

3. Calculate Your Total Cost: Add fund fees, advisory fees, account maintenance charges, and transaction costs. If the total exceeds 1.5% annually, you’re likely overpaying.

4. Seek Clean Share Advisors: Look for CGP or CIF (conseiller en investissement financier) who offer transparent fee structures without retrocessions. They exist, though they’re in the minority.

5. Read the Fine Print: Those thick assurance-vie contracts and fund prospectuses contain fee details, but you must dig. The 2% management fee is just the beginning.

The Inevitable Reckoning

The ESMA data makes one thing clear: the current fee split is unsustainable. As French investors become more sophisticated and international comparison tools more accessible, pressure for transparency will only increase. Banks defending the retrocession model are fighting a losing battle against arithmetic.

The question isn’t whether France will eventually reform its fund distribution model, it’s whether you’ll still be paying these hidden fees when change finally comes. Your 2% annual gain shouldn’t be a commission split between your fund manager and your bank. It should be actual profit in your pocket.

Until then, every time you review your investment statement, remember: that line showing “ongoing charges” is likely hiding a 50/50 split where your banker gets paid just as much as the investment professional, regardless of whether your portfolio goes up or down. In what other business does the salesperson earn as much as the expert actually doing the work?