Smartbroker’s Crisis Marketing: When German Fintech Turns Geopolitical Chaos Into Profit

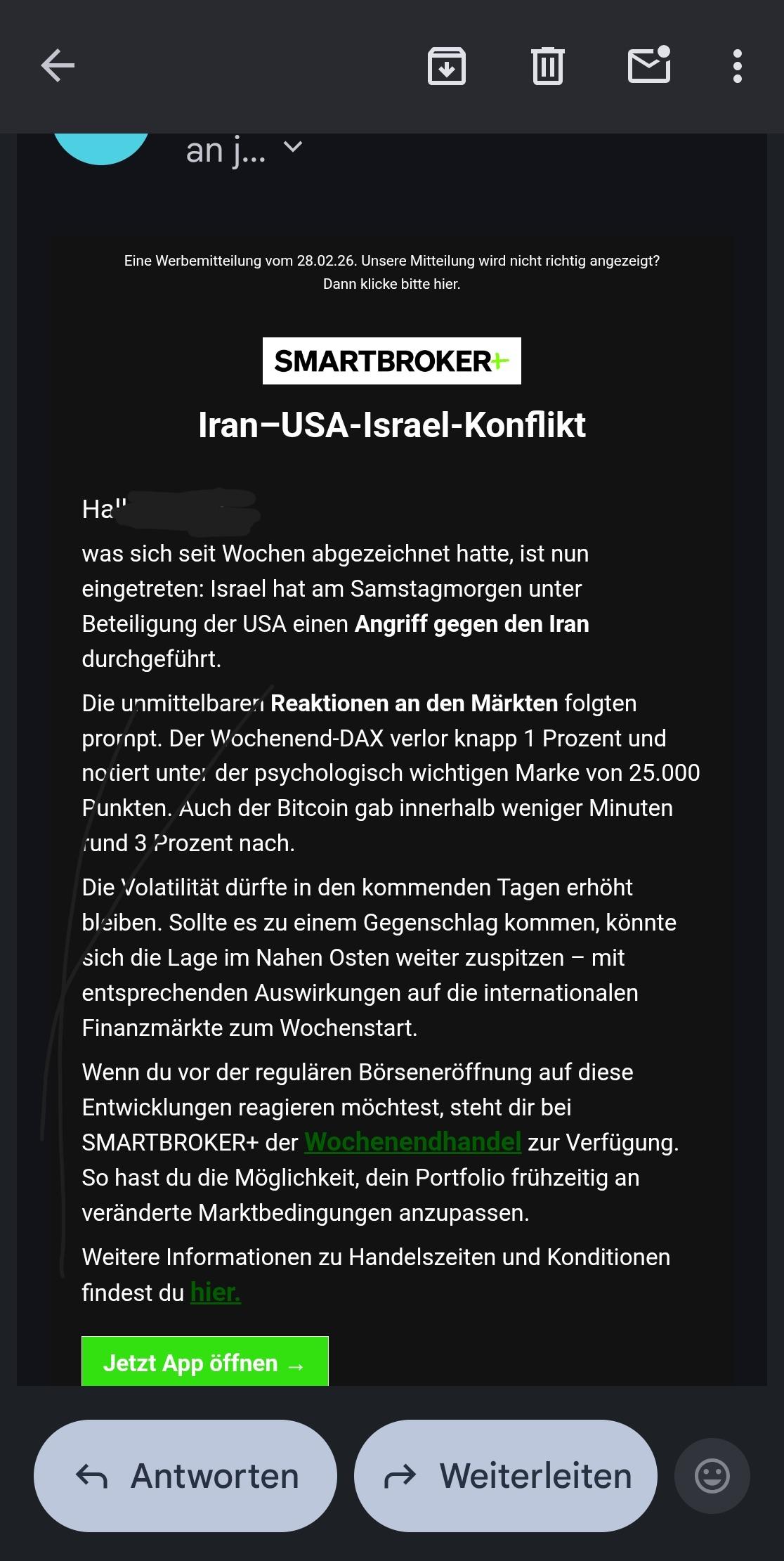

The notification landed on German phones like a digital ambulance chaser: while missiles flew and markets convulsed over Iran, Smartbroker+ saw not a humanitarian crisis, but a sales opportunity. Their advertisement promoting Wochenendhandel (weekend trading) during the opening salvos of geopolitical instability didn’t just cross a line, it erased it entirely. This isn’t just about bad taste, it’s a case study in how Germany’s fintech disruptors are importing Silicon Valley’s “move fast and break things” ethos into spaces that demand sober responsibility.

The Anatomy of a Crisis Marketing Misfire

Within hours of Iran-related market turbulence, Smartbroker+ pushed notifications framing volatility as a feature, not a bug. The message was clear: while the world watched escalating conflict, you could be trading. Many international residents in Germany’s investor community reacted with visceral discomfort, calling the move everything from tone-deaf to exploitative. The sentiment wasn’t just about propriety, it reflected a deeper concern that Krisenmarketing (crisis marketing) had officially arrived in German retail investing.

The timing proved particularly galling. Geopolitical analysts had tracked rising tensions for days, yet the marketing materials appeared with suspicious speed. This suggests either a remarkably agile marketing team or, more troubling, pre-approved campaigns waiting for the right crisis trigger. For a financial institution operating under Germany’s strict regulatory framework, the latter scenario raises serious questions about internal compliance and ethical oversight.

Why Weekend Trading During Crises Is Financially Reckless

Beyond the ethical failure lies a practical problem: weekend trading during geopolitical shocks is a retail investor trap. German neobrokers like Smartbroker+ offer extended hours, but these come at a steep cost that marketing glosses over.

Liquidity evaporation turns weekend markets into minefields. When institutional traders are offline, bid-ask spreads balloon dramatically. What looks like a 2% price movement might hide a 3% spread, meaning you’re underwater the moment you click “buy.” Many German investors learned this the hard way during previous crises, finding themselves panic-selling into illiquid markets with no Handelsplatz (trading venue) depth.

The Smartbroker+ promotion essentially encouraged this behavior, transforming legitimate concern about global events into transaction revenue. While the broker profits from each trade regardless of outcome, customers face amplified risks in already chaotic conditions. This is the opposite of Anlegerschutz (investor protection), a core principle of German financial regulation.

The German Regulatory Blind Spot

Germany’s BaFin (Federal Financial Supervisory Authority) has aggressively pursued traditional banks for misconduct, from banks profiting from institutional failure and customer vulnerability to questionable public bank trust versus profit-driven debt strategies. Yet fintech marketing practices often slip through regulatory cracks.

The Smartbroker incident reveals a critical gap: BaFin scrutinizes product disclosures and fee structures, but marketing ethics during crises remains ambiguous territory. While traditional German banks like Sparkasse maintain conservative, almost stodgy messaging, neobrokers operate with the speed and moral flexibility of social media platforms. This asymmetry creates a race to the bottom where established players may feel pressure to match the fintechs’ aggressive tactics.

German law requires financial advertisements to be “langemessen” (appropriate), but defining appropriateness during geopolitical crises is subjective. The Finanzvermittlungsverordnung (Financial Intermediary Ordinance) focuses on transparency, not timing or taste. This loophole allows brokers to legally exploit panic, even if it violates the spirit of investor protection.

Systemic Patterns in German Fintech Marketing

Smartbroker+ isn’t an isolated case, it’s part of a broader pattern where German fintechs prioritize user acquisition over fiduciary duty. The industry has normalized several problematic approaches:

1. Democratization narratives that mask risk. Like critiquing broker narratives around accessible private market investments, crisis marketing frames dangerous products as empowerment. “Now everyone can trade like a professional” sounds liberating until you realize professionals have risk management teams and you’re trading alone at midnight.

2. Feature-first, consequence-later messaging. The focus on Wochenendhandel (weekend trading) highlights capability without warning about amplified spreads, emotional decision-making, or the statistical reality that most retail traders lose money during volatile periods. It’s like advertising a car’s top speed without mentioning brakes.

3. Agility as ethical exemption. Fintechs claim their speed requires regulatory flexibility, but this often becomes moral flexibility. When examining how revenue models impact investor protection in fintech, we see that even positive changes (like ditching Payment-for-Order-Flow) don’t automatically create ethical marketing cultures.

The Psychological Toll on German Investors

Living in Germany means navigating financial decisions within a culture that values stability and long-term thinking. The Sparbuch (savings account) mentality still influences investor psychology, even among younger, app-savvy Germans. Crisis marketing exploits this cultural tension, triggering fear in people trained to avoid risk.

Many international residents report feeling particularly vulnerable. Unfamiliar with German consumer protection mechanisms and often isolated from family support networks, they’re more likely to make impulsive decisions when crisis notifications light up their phones. The Smartbroker+ ad didn’t just target investors, it targeted scared humans.

The aftermath follows a predictable pattern: trades placed in panic, losses realized by Monday, and a support system that’s digital-only when human empathy is most needed. This mirrors demonstrating real consequences when fintech promises fail investors, where technological convenience becomes a liability during actual crises.

What Ethical Crisis Communication Looks Like

German financial institutions have a responsibility to do better, both legally and morally. Ethical crisis communication follows three principles:

- 1. Silence is golden. During the initial shock of geopolitical events, brokers should pause promotional activity. This isn’t censorship, it’s respect. Deutsche Bank and Commerzbank historically maintain radio silence during major crises, letting markets function without their commentary.

- 2. Education over exploitation. If brokers must communicate, the message should focus on risk management, not opportunity. “Understanding volatility” beats “trading volatility” every time. This aligns with Germany’s Verbraucherbildung (consumer education) mandates.

- 3. Systemic safeguards. Platforms should automatically disable promotional notifications during major geopolitical events, just as they halt trading during technical glitches. This removes temptation and protects both investors and the broker’s reputation.

Investor Self-Defense in the Notification Age

German investors, both locals and international residents, need proactive strategies:

- Disable push notifications for trading apps. Treat them like slot machines: designed to trigger action, not reflection. Check markets on your schedule, not when an algorithm decides.

- Establish a “crisis checklist.” Before trading during any geopolitical event, answer: Am I acting on analysis or emotion? Is this in my investment plan? Would I explain this trade to the Finanzamt (Tax Office) next year?

- Understand your broker’s incentives. When evaluating marketing claims versus actual data utility in finance apps, remember: if you’re not paying for the product, you are the product. Weekend trading spreads and payment-for-order-flow arrangements mean your panic is their profit.

The Bottom Line

Smartbroker+ didn’t just make a marketing mistake, it revealed a cultural shift in German fintech where user engagement metrics trump investor welfare. The company’s rapid-response promotion during the Iran crisis treated geopolitical instability as a Gewinnchance (profit opportunity), reducing complex global events to a conversion funnel.

For Germany’s financial ecosystem, this serves as a warning. The BaFin must expand its oversight beyond product features to include marketing timing and tactics. Traditional banks should resist the urge to match fintech aggressiveness. And investors must recognize that the most dangerous time to trade is when your broker tells you it’s urgent.

The missiles over Iran weren’t a marketing opportunity. They were a humanitarian crisis. Any German financial institution that can’t tell the difference deserves not just regulatory scrutiny, but customer exodus. In a market built on trust and long-term thinking, crisis marketing isn’t just tasteless, it’s financial self-harm.

Actionable Takeaway: Review your broker’s notification settings this week. If they sent you promotional messages during recent geopolitical events, consider switching to a provider that respects the difference between market volatility and human tragedy. Your portfolio, and your conscience, will thank you.