Is Finanzguru Worth It? The Truth Behind Germany’s Popular Financial Optimization Tool

Finanzguru promises to slash your insurance costs and organize your financial life, but a growing chorus of German users wonders if it’s just another data vacuum with a slick interface. The app has sparked heated debates across financial communities, with supporters calling it indispensable and skeptics warning it’s a solution in search of a problem. Let’s cut through the marketing and examine what this tool actually delivers.

The Core Promise: What Finanzguru Actually Does

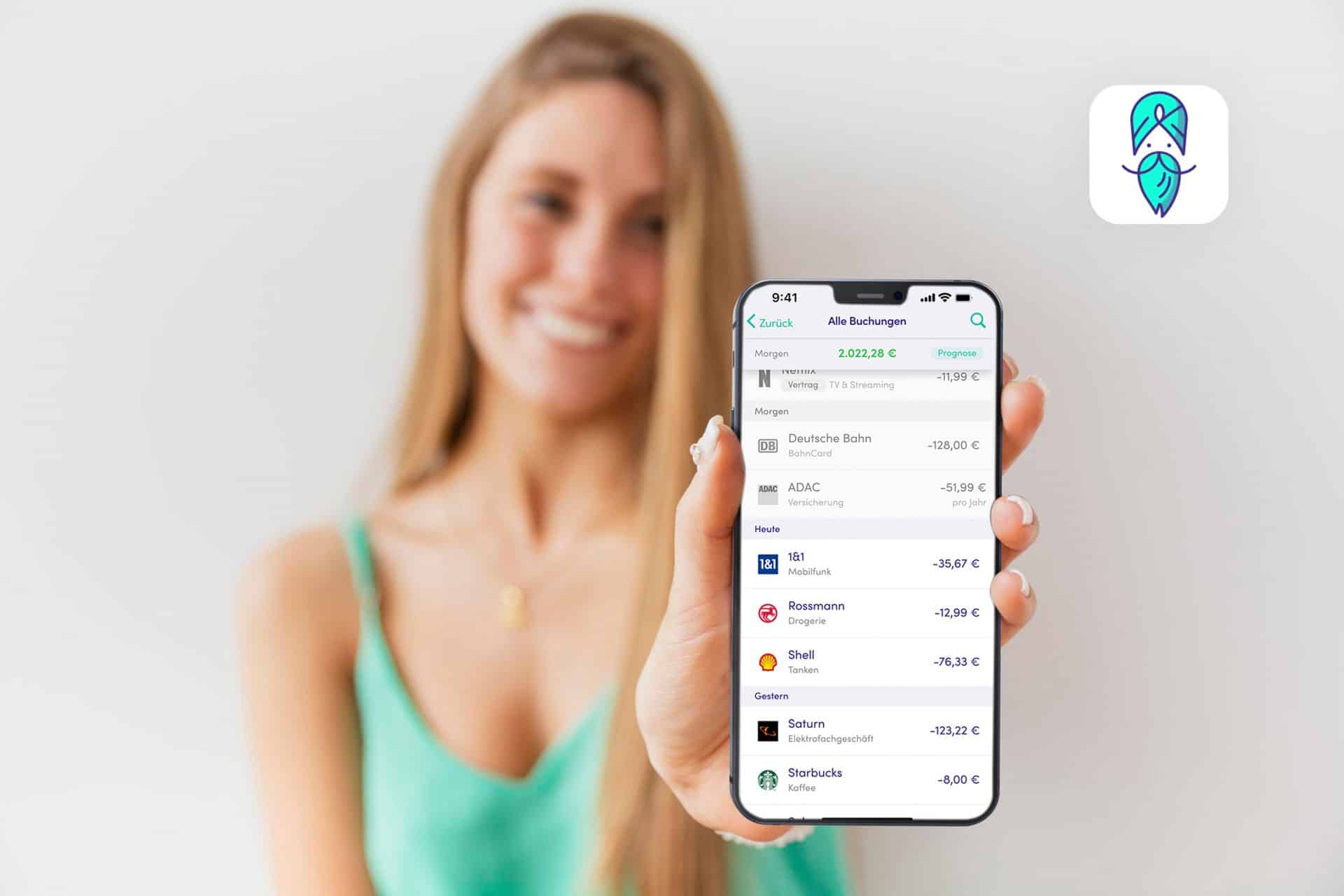

At its heart, Finanzguru functions as a digital financial assistant that aggregates your accounts, tracks spending, and identifies potential savings. The free version handles basic multi-banking, automatically categorizes transactions, and provides a unified dashboard for your financial life. You connect your Girokonto (checking account), credit cards, PayPal, and even investment accounts to get a complete picture.

The Plus version, which typically costs €2.99 monthly (though some users report seeing €3.99), unlocks extended analytics, CSV export functionality, and more sophisticated budgeting tools. For many, the upgrade transforms the app from a simple expense tracker into a proactive financial management system.

The real selling point, however, is the Versicherungscheck (insurance check). Finanzguru scans your contracts and suggests cheaper alternatives, potentially saving hundreds annually on policies like Haftpflichtversicherung (liability insurance) or Kfz-Versicherung (car insurance). This feature alone convinces many users that the subscription pays for itself.

The Maklermandat Controversy: When "Help" Becomes a Takeover

Here’s where the story takes a turn. Finanzguru offers to manage your insurance contracts directly, but this requires signing a Maklermandat (broker mandate). Once granted, Finanzguru becomes your official insurance broker, which means your previous local agent loses access to your policies.

Critics warn this creates a dangerous dependency. If you have a complex Schadensfall (damage claim), you might find yourself dealing with a digital platform instead of a personal contact who knows your history. One user reported that after granting the mandate, their local Versicherungsvertreter (insurance agent) could no longer assist them, leaving them stranded during a claim.

The company insists the mandate is optional and only applies to contracts you explicitly approve. Yet many users report feeling pressured to grant broad permissions, and the interface doesn’t always make the opt-out path obvious. This mirrors patterns seen in other German financial services where convenience often comes with hidden control shifts, similar to how loyalty penalties in banking services can quietly erode your returns.

Data Privacy: Germany’s Favorite Anxiety

Germany’s relationship with data privacy is complicated. We obsess over the Impressum (legal notice) on websites yet freely upload our financial lives to apps. Finanzguru stores data in German servers under BaFin supervision, which reassures some users but leaves others unconvinced.

The fundamental question: why trust a third party with your complete financial picture? Skeptics argue that anyone needing an app to track spending has already lost control of their finances. Supporters counter that modern life involves too many accounts, subscriptions, and contracts to manage manually.

The platform’s business model adds another layer of concern. Finanzguru earns commissions when you switch insurance providers through their recommendations. This creates an inherent conflict: are they suggesting the best policy for you, or the one with the highest commission? This tension between user benefit and revenue generation echoes debates about hidden investment fees eroding returns.

Real-World Performance: The User Sentiment Spectrum

Dig into user experiences and you’ll find a bipolar distribution. Long-term users frequently describe Finanzguru as "unverzichtbar" (indispensable), praising how it reveals spending patterns they’d never noticed. One user mentioned discovering €60 in forgotten subscriptions within the first week.

Power users with multiple accounts appreciate the centralized view, though some report that frequent transfers between their own accounts can confuse the algorithm, miscategorizing them as income. The workaround, manually marking transactions as internal transfers, exists but requires initial setup effort.

Critics fall into two camps: privacy fundamentalists who reject any financial aggregation, and spreadsheet purists who find Excel more flexible. Several users switched to alternatives like Finanzblick (by Buhl) or Outbank, citing better categorization or tax preparation features. Finanzblick, for instance, integrates directly with Wiso tax software and lets you attach receipts to transactions, a feature Finanzguru lacks.

The Three-Month Trap: Promotional Pricing Psychology

Both Neukunden (new customers) and existing users can currently test Plus for three months free using codes like "CONTROL26" or "REISEN25." This strategy mirrors German magazine subscription tactics, hook users with a deal, then rely on inertia to convert them to paying customers.

The psychology works. Many users admit they signed up for the trial and stayed because canceling felt like too much effort. At €2.99 monthly, it’s priced below the "pain threshold" where people actively review subscriptions. This is precisely how comparing financial tools for cost savings often reveals that convenience comes with a recurring price tag.

When Finanzguru Actually Makes Sense

The app delivers clear value for specific user profiles:

- The Overwhelmed Expat: If you’re new to Germany and drowning in unfamiliar insurance requirements, contract terms, and banking fees, Finanzguru provides a crash course in your own financial life. The automatic categorization helps you understand where your money goes without mastering German financial vocabulary first.

- The Subscription Collector: Germans average 7-12 recurring subscriptions. If you can’t list yours from memory, Finanzguru’s contract detection is genuinely useful. One user reported saving €240 annually by canceling duplicate streaming services and forgotten gym memberships.

- The Insurance Optimizer: For those who haven’t shopped for insurance in years, the Versicherungscheck can identify outdated premiums. However, the savings diminish after the first year, you can’t keep switching providers annually without consequences.

- The Multi-Banking Power User: If you maintain accounts at Sparkasse, Deutsche Bank, and multiple online banks, the unified view saves time. But be prepared to spend an hour initially training the categorization system.

The Hidden Cost of "Optimization"

Finanzguru’s true cost isn’t monetary, it’s the mental shift toward algorithmic financial management. The app encourages you to outsource decision-making about contracts and insurance to its commission-driven recommendations. Over time, this can erode your financial literacy rather than build it.

Moreover, the platform’s business model depends on you remaining a passive consumer. The more actively you manage your finances, the less you need Finanzguru. This creates a paradox: the app is most valuable to those who need it least, and potentially harmful to those who need it most.

Users who rely entirely on the app’s recommendations without understanding their insurance needs might end up underinsured. A cheaper policy isn’t better if it excludes critical coverage. Your local agent, despite potential bias, at least knows your personal circumstances.

Verdict: Worth It, But Only on Your Terms

Finanzguru is neither scam nor savior. It’s a tool whose value depends entirely on your financial complexity and personal discipline.

- Get the free version if you want better spending visibility and don’t mind spending an hour setting up categories. It’s genuinely useful for tracking expenses and spotting forgotten subscriptions.

- Try Plus for three months using a promotional code, but set a calendar reminder to cancel before automatic billing kicks in. Use the trial to export your data and analyze spending patterns, then decide if the insights justify the cost.

- Avoid the Maklermandat unless you fully understand what you’re giving up. Keep your insurance relationships direct, and use Finanzguru purely as an information tool, not a decision-maker.

- Consider alternatives if you need tax integration (Finanzblick) or prefer a more established banking app (Outbank). The German fintech market is crowded, and loyalty rarely pays, just as loyalty penalties in banking services demonstrate.

The ultimate truth? Finanzguru excels at showing you where your money goes but can’t teach you how to care about it. For that, you still need old-fashioned financial literacy, no app can replace understanding the difference between Riester-Rente (Riester pension) and ETF-Sparplan (ETF savings plan), or why your Kaution (rental deposit) should sit in a separate account.

Use Finanzguru as a mirror, not a map. Let it reflect your financial reality, but don’t let it chart your course.