The Swiss Marriage Tax Penalty: How Couples Lose 1 Million CHF and Why Divorce Looks Rational

The Swiss tax system operates with the same reliability as an SBB train, usually impeccable, until construction slows the line. For married couples, that construction zone is called the Heiratsstrafe (marriage penalty), and the delays cost some families up to one million Swiss francs over a lifetime.

Jan, a 34-year-old father in a leadership position, learned this the hard way. After six years of marriage, he ran the numbers and discovered his family would pay roughly CHF 1 million less by retirement if he and his wife divorced, calculating lost investment returns at 5% annually. “We love each other, we’re a happy family, but rationally, we should get divorced”, he told 20 Minuten.

This isn’t hyperbole. It’s math.

How the Marriage Penalty Actually Works

Switzerland’s progressive tax system means higher incomes face steeper rates. The federal constitution mandates taxation “according to economic capacity”, which sounds fair until two incomes become one in the eyes of the Steueramt (Tax Office).

For unmarried couples, each partner files separately. Two salaries of CHF 80,000 get taxed in lower brackets. For married couples, incomes merge. That CHF 160,000 household income jumps into a brutally higher tax bracket.

The federal tax formula illustrates this clearly: a single person earning CHF 100,000 pays roughly 3% federal tax. A married couple earning CHF 200,000 pays about 6%. Same income per person, double the rate.

The penalty formula is simple: Marriage Penalty = Tax(married, x+y) – [Tax(single, x) + Tax(single, y)]

Where x and y are each spouse’s income. When both partners earn more than CHF 20,000 annually, the federal penalty kicks in. For middle-class dual earners, it can exceed CHF 12,000 per year, or over 3.5% of total household income.

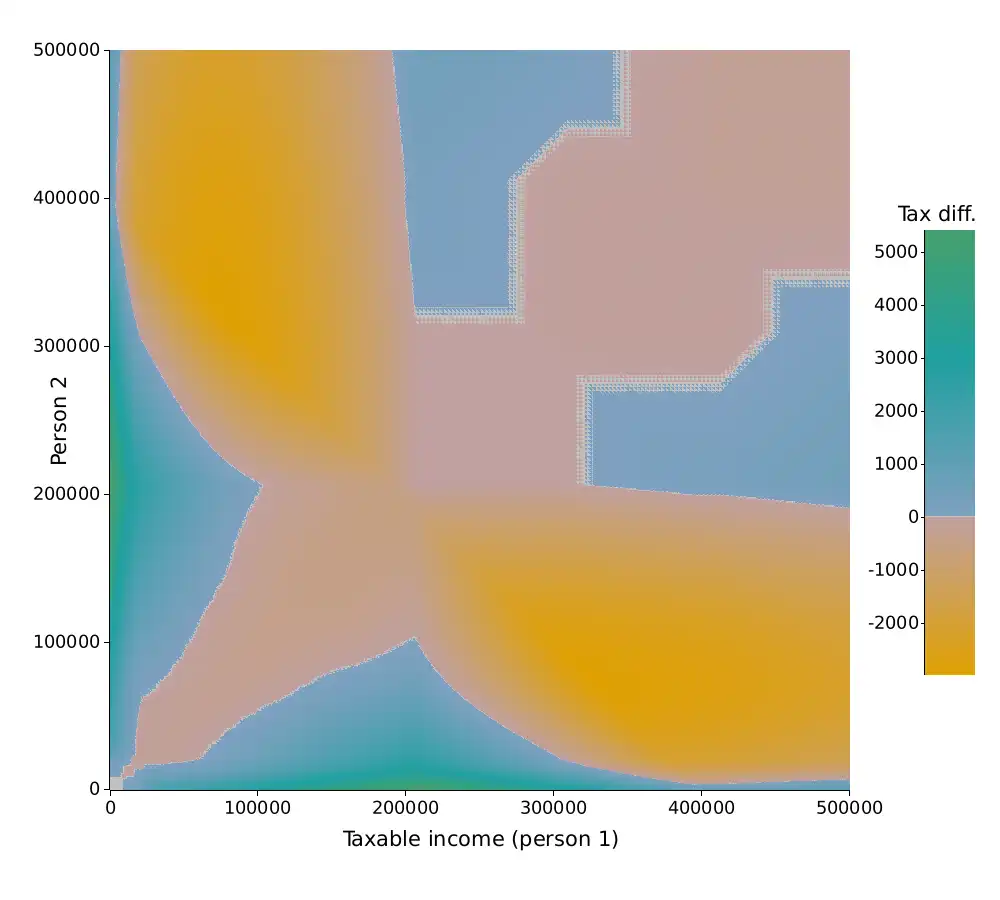

Cantonal Chaos: Where You Live Determines Your Loss

Here’s where Swiss federalism turns into a financial lottery. Each of the 26 cantons plays by different rules, creating bizarre outcomes where moving 10 kilometers can save you thousands.

- Fribourg: Uses splitting factor of 2.0—equal earners pay same tax married or not, but divergent incomes create penalties

- Geneva: Rewards marriage with Heiratsbonus exceeding CHF 12,000 annually, except when incomes are perfectly equal

- Zurich & Ticino: Moderate penalties around 1% of income for dual earners

- Neuchâtel: Produces bird-shaped penalty pattern—similar incomes pay slightly more, vastly different incomes pay substantially more

The takeaway? Your cantonal tax code matters as much as your wedding vows. Some couples in Geneva are financially incentivized to marry, while their counterparts in Zurich calculate divorce savings.

Real-World Damage: Numbers That Hurt

Let’s quantify the actual pain with verified cases:

Jan’s Family

Pays CHF 36,000 annually as a married couple. Would pay under CHF 26,000 unmarried. Difference: CHF 10,000+ per year.

Marek (47)

Dual-income couple pays CHF 8,000 more yearly. Also faces reduced AHV pensions since married couples max out at 150% of a single pension.

Sabrina (36)

Childless couple pays CHF 5,000 extra annually simply for having a marriage certificate. “We get punished for not having kids”, she says.

The median Swiss salary is CHF 84,288. For a couple each earning this amount, the federal penalty alone reaches CHF 6,000+ annually. Over 30 years with compound investment returns, that’s CHF 400,000+ in destroyed wealth, not counting cantonal penalties.

The Individualbesteuerung Vote: A Political Tightrope

On March 8, 2026, ironically International Women’s Day, Switzerland votes on Individualbesteuerung (individual taxation). The reform would require each spouse to file separately, eliminating the marriage penalty at federal and cantonal levels.

Polls show a nervous 52-53% support, down from 64%. Why the hesitation?

📊 The Yes Argument

- 50% of taxpayers would pay less, only 14% would pay more

- Dual-income couples gain CHF 600 million in relief

- Removes systematic disadvantage against second earners, predominantly women

- Creates incentives for skilled professionals to work full-time amid labor shortage

⚠️ The No Argument

- Traditional single-earner families would pay CHF 670+ more annually

- Reform “attacks marriage” and creates bureaucracy

- 1.7 million additional tax returns required

- Cantons fear implementation costs of CHF 130 million

The political alliance is unusual: left parties (SP, Greens) join the free-market FDP to support the reform, while the conservative SVP and Mitte-Partei oppose it. Some SP veterans even defect, warning of “new inequalities.”

Actionable Strategies: What Couples Can Do Now

While waiting for the vote, couples have options:

1. Delay the Wedding

If you’re both high earners, consider waiting. The financial difference between December 31 and January 1 nuptials can be five figures.

2. Optimize Your Canton

The data shows massive cantonal variation. Moving from a high-penalty canton to a bonus canton like Geneva can offset the marriage penalty entirely. For remote workers, this is a legitimate strategy.

3. Leverage the 3rd Pillar

Maximize Säule 3a (Third Pillar) contributions. While this doesn’t eliminate the penalty, it reduces taxable income at both federal and cantonal levels. Couples can contribute up to CHF 7,056 each in 2025.

For more on how individual taxation affects singles differently, see individual taxation reform and singles tax burden.

4. Consider Employment Structures

Some couples explore hiring one spouse by the other’s company to split income more favorably. This falls into legal gray areas discussed in marriage penalty and tax avoidance strategies.

5. Calculate Your Exact Penalty

Use the federal tax calculator or third-party tools to model your specific situation. The difference often justifies professional tax advice, which costs less than one year’s penalty.

The Divorce Calculation

When couples seriously consider divorce for tax reasons, the system has failed. But the math is undeniable:

Example: A couple each earning CHF 120,000 in Zurich pays approximately CHF 8,500 more annually in federal and cantonal taxes than unmarried partners. Invested at 5% over 30 years, that’s CHF 560,000 in lost wealth.

Add the AHV pension reduction (married maximum 150% of single pension vs. two full single pensions) and the lifetime cost exceeds CHF 1 million for high earners.

As Jan notes: “We chose an equal partnership, in careers and childcare. We’re punished for it.”

The Bigger Picture: Systemic Inefficiency

The marriage penalty doesn’t just hurt feelings, it distorts economic behavior. Switzerland faces a skilled labor shortage, yet the tax system discourages second earners, mostly highly educated women, from full-time work.

Jamie Vrijhof-Droese, a wealth manager and author, argues: “A tax system should be neutral toward life models.” The current system fails this basic principle, creating perverse incentives that cost the economy thousands of skilled workers.

Moreover, the penalty complicates estate planning. Married couples estate planning becomes more complex when tax considerations override relationship stability.

What Happens Next?

If the March 8 vote passes, implementation takes six years. Couples would file individually, but must still divide assets and deductions equitably. The bureaucracy concern is real, 1.7 million new tax returns represent a one-time shock.

If it fails, the marriage penalty persists. Some cantons may continue solo reforms, deepening the geographic lottery. The pressure for change won’t disappear, it will simply shift to the next referendum cycle.